This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Health savings accounts (HSA) provide another vehicle to save for retirement. Many of you have the option to enroll in high-deductible insurance plans that allow the use of a health savings account via your employer. High deductible health insurance plans . Your HSA can be another leg on the retirementplanning stool.

30 years ago, when financial plans relied mainly on constant investment return projections derived from straight-line appreciation and time-value of money calculations, financial advisors began acknowledging and accounting for the variable and uncertain nature of investment returns. Read More.

This month's edition kicks off with the news that Riskalyze has completed its previously-announced rebranding, and will now be known as “Nitrogen”, a ”growth platform” for advisory firms – which represents less of a shift in the platform’s core function (given that Riskalyze’s risktolerance tool was always (..)

30 years ago, when financial plans relied mainly on constant investment return projections derived from straight-line appreciation and time-value of money calculations, financial advisors began acknowledging and accounting for the variable and uncertain nature of investment returns. Read More.

Historically, advisors haven't had many avenues to manage clients' 401(k) plan accounts, since unlike traditional custodial investment accounts, advisors generally lack discretionary trading authority in employer-sponsored retirementplans.

Historically, advisors haven't had many avenues to manage clients' 401(k) plan accounts, since unlike traditional custodial investment accounts, advisors generally lack discretionary trading authority in employer-sponsored retirementplans.

Among these are your longevity, lifestyle, comfort with market performance, sequence of return risk, current health, housing plan, proportion of fixed to variable expenses, proximity to children and so much more. One or two million dollars may seem like a lot of money to have set aside for retirement. A Retirement Reality Check.

Assuming that you have a financial plan with an investment strategy in place there is really nothing to do at this point. Ideally you’ve been rebalancing your portfolio along the way and your asset allocation is largely in line with your plan and your risktolerance. Focus on risk. Do nothing. Look for bargains.

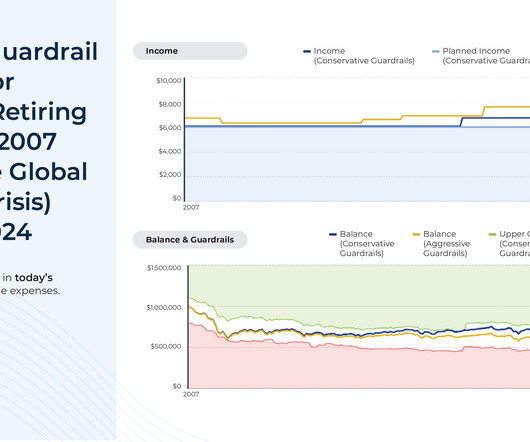

Monte Carlo simulations have become a central method of conducting financial planning analyses for clients and are a feature of most comprehensive financial planning software programs. a client who really wanted to guard against downward-spending-adjustment-risk might forgo income increases entirely). Read More.

Last year’s considerable losses and market fluctuations underscore the need for clients to assess their retirementplans to ensure it aligns with their objectives, financial situations, timelines, and attitudes toward market volatility. You can help them start the year right by conducting a retirement checkup.

The choice between stocks and bonds depends on their individual circumstances, such as risktolerance, time horizon, and financial goals. While an investor’s timeline affects their risktolerance and allocation decisions between stocks and bonds, it’s important to remember how long a retirement time horizon can truly be.

Rather I suggest an investment strategy that incorporates some basic blocking and tackling: A financial plan should be the basis of your strategy. Any investment strategy that does not incorporate your goals, time horizon, and risktolerance is flawed. Take stock of where you are. Photo credit: Flickr.

For example, your plan might call for a 60% allocation to stocks but with the gains that stocks have experienced you might now be at 70% or more. This is great as long as the market continues to rise, but you are at increased risk should the market head down. Financial Planning is vital. Click To Tweet.

While grappling with various aspects of retirementplanning, it is imperative to acknowledge a critical factor that often does not receive its due attention – longevity risk. Longevity risk refers to the risk that people are living longer lifespans than previous generations.

For one person, that might mean reassessing their risktolerance and portfolio holdings to make sure that they hold assets that will at least sustain their value or provide a safer return, such as an interest rate or a dividend yield. What Can We Expect from the Markets? Why Meet with a Financial Advisor?

This advanced language processing technology has also greatly impacted the financial advisory sector, prompting a critical question: Can ChatGPT replace human financial advisors in retirementplanning? Personalized guidance, empathy, and a deep contextual understanding are integral to effective retirementplanning.

The answer to “how much you need to retire” is shaped by various factors, including the kind of retirement life you dream of, your age, and the expenses you anticipate during your retirement years. Retirementplanning is not just about reaching a target savings number.

No one cares about your financial well-being more than you, so it's important to have a financial plan for yourself. Knowing how to make a financial plan will allow you to save money, afford the things you really want, and achieve long-term goals like saving for college and retirement. What is a financial plan?

The Roth IRA vs traditional IRA – they’re basically the same plan, right? While they do share some similarities, there are enough distinct differences between the two where they can just as easily qualify as completely separate and distinct retirementplans. Not exactly. The most basic requirement is that you have earned income.

Depending on your income goals and risktolerance, this bucket can provide you with dividend or interest income that can supplement other forms of retirement income. During working years, this bucket is less of a concern, but come retirement, planning your income sources to fund this bucket is crucial.

Traditional IRA: Best for Dedicated RetirementPlanning. IRA plans are subject to Required Minimum Distributions (RMDs) beginning at age 72. Roth IRA: Best for RetirementPlanning + Immediate Funds Access. Same procedure as with traditional IRAs, except you must specify the plan will be a Roth. Ads by Money.

And how does it compare to the 401k and other retirementplans that exist? A Simple IRA, or Savings Incentive Match Plan for Employees, is a type of employer-sponsored retirement savings plan that is designed to be easy to set up and maintain for small business owners. What is a Simple IRA?

Meeting with a qualified financial planning professional can help you begin building positive and lasting behaviors.?? . Take Advantage of RetirementPlans and Matching Contributions. Employers often match a portion of this contribution to a retirementplan as an employer benefit. . Million after 40 years!

This data can serve as a baseline for tailoring your retirementplan, taking into account factors such as inflation, your current age, and your desired retirement age. These figures can serve as a valuable reference point for individuals planning their retirement.

When we are busy working to earn a living and spending time with our family, first thing needs to think about is RetirementPlanning. Generally, people think about Retirementplanning after retirement. To plan for retired life important thing is financial plan.

No one cares more about your financial well-being than you, so having a personal financial plan is important. Knowing how to make a financial plan will allow you to save money, afford the things you want, and achieve long-term goals like saving for college and retirement. Table of contents What is a financial plan?

1] What are Your Investment Goals and RiskTolerance When selecting investments for your IRA, consider your investment goals and risktolerance. Your goals may be different depending on your age, retirement timeline, and lifestyle.

Are you good with numbers, accounting, and financial planning? If yes, then DIY financial planning might be a good option for you. On the other hand, if you tend to struggle with budgeting or find financial planning overwhelming, then professional money management could be a better solution. What is DIY financial planning?

High yields can be a sign of underlying issues with the company that puts principal at risk and endangers the dividend income if the company’s financials cannot support it. Before you can evaluate stocks or bonds to invest in, you’ll need to develop the metrics you plan to use in the analysis. versus 1.1%

Retirement is an exciting milestone—a time to leave behind the hustle and bustle of work and embrace a new chapter filled with more freedom and opportunities to enjoy life. Planning well in advance ensures that your retirement years will be financially secure, fulfilling, and less stressful than your working years.

A lot of people out there dream of early retirement – who wouldn’t love to hang up the office keys and jump off the 9-5 train sooner rather than later? But while it’s possible to retire at 50 and have plenty of time left in life to have new experiences, it takes careful planning and a will of steel.

Whether planning for retirement, saving for your children’s education or simply looking to grow your investments, finding the right wealth management services in Kansas City can make all the difference. Long-term goals typically encompass retirementplanning, wealth preservation and estate planning.

So, let’s discuss how to save for retirement in your 20s! Table of contents Why saving for retirement early matters 1. The 401(k) Plan 2. Here’s what happens when you take money out of your retirement account How to avoid withdrawing money early Should I roll over my old 401k to my new employer’s plan?

A Guide for Financial Planning When it comes to managing your finances, it’s crucial to work with a professional who puts your interests first. As a result, this plan can help guide your financial decisions and ensure that you’re on track to achieve your goals. The post What’s a Fiduciary & Fee-Only Advisor?

You may consult with a professional financial advisor to better understand your financial history and the ensuing impact your past choices may have on your future financial planning. They provide an opportunity to make necessary adjustments, whether it’s reallocating investments, revisiting saving rates, or redefining retirementplans.

According to the Department of Labor , “Based on the experience of Council members, and testimony and conversations with recordkeepers, the value of uncashed retirementplan checks likely exceeds $100 million per year but could be considerably larger.

The investment service includes access to dedicated financial advisors and assistance with managing your employer-sponsored retirementplan. Investment advice for employer-sponsored retirementplans. Vanguard funds are among the most popular in the world. Check out my Personal Capital review for more information.

Whether planning for retirement, saving for your children’s education or simply looking to grow your investments, finding the right wealth management services in Kansas City can make all the difference. Long-term goals typically encompass retirementplanning, wealth preservation and estate planning.

We all know retirement is an important milestone that requires careful planning. Of course, one of the most important aspects of retirementplanning is managing retirement taxes. Taxes can significantly impact the amount of money you’ll have for retirement.

We all know retirement is an important milestone that requires careful planning. Of course, one of the most important aspects of retirementplanning is managing retirement taxes. Taxes can significantly impact the amount of money you’ll have for retirement.

In most cases, you plan for little involvement on your part once you’ve invested the money. Then you can choose the options that are best for you when you create your investment portfolio and financial plan. Leverage tax-advantaged retirement savings accounts from your employer first. Prepare with your risktolerance in mind.

I also owned the name for a couple of more risktolerant clients. For a ten year run ending Jan 1, 2019 though it compounded at over 6% annually plus that dividend yield on top and a very low beta. To me, that was a great mix of attributes. At some point along the way I lost faith in China from the top down and sold it.

Your investment strategy determines the target percentages for each asset, often based on your risktolerance, investment goals, and time horizon. This may lead to a higher or lower risk profile than initially intended. With a higher income, your risktolerance can increase, and you may be more open to investing in equities.

In most cases, you plan for little ongoing involvement on your part once you’ve invested the money. Then you can choose the options that are best for you when you create your investment portfolio and financial plan. Create your plan for investing Next, it’s time to sit down and create your basic plan for investing.

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content