This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

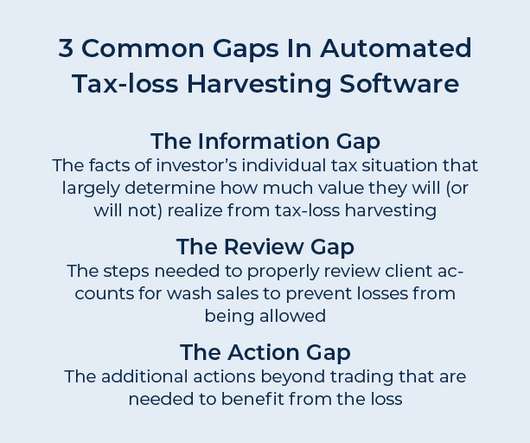

In recent years, numerous software solutions have sprung up that aim to automate the process of tax-loss harvesting. But what the providers of automated tax-loss harvesting often don’t mention is that the actual value of tax-loss harvesting depends highly on an individual’s own tax circumstances.

Welcome to the October 2023 issue of the Latest News in Financial #AdvisorTech – where we look at the big news, announcements, and underlying trends and developments that are emerging in the world of technology solutions for financial advisors!

Tax-loss harvesting is a powerful strategy that investors can use to reduce their taxable income. This type of strategy typically involves selling underperforming investments at a loss to offset capital gains (or ordinary income) to optimize portfolio returns. Table of Contents What is tax-loss harvesting?

Advisors are being asked to provide their clients with a full suite of solutions, ranging from estate and taxplanning to portfoliomanagement, and everything in between. Clients are increasingly eager to gain access to fully customizable solutions that meet their individual needs.

A financial advisor can help you with portfoliomanagement, risk reduction, and inflation protection During retirement, your investment goals shift from accumulation to preservation of wealth. Your investment risk appetite is lowered, and it is important to readjust your portfolio accordingly.

Topics will included: • How to structure the earn out. • Creating a diversification plan from a large single stock position • What are some of the key logistical issues to be aware of and how can you navigate them?

Speakers: Michael Aldrich, Global Head of Operational Security; Rebecca Sugarman, Chief Human Resources Officer; Craig Standish, Head of Boston Office Moderator: Victor Abiamiri, PortfolioManager. . Planning for Your Liquidity Event and Beyond. MORE ON THIS TOPIC Strategic Planning Roadmap for Entrepreneurs.

The Evolution of Financial Planning The financial planning industry has transformed significantly over the past decade. Modern financial planners must navigate complex investment products, understand evolving tax regulations, and adapt to technological innovations.

Tax Considerations Be mindful of tax implications related to your goals. Certain investments or strategies may offer tax advantages, while others could result in higher tax liabilities. Consulting with an advisor can help you optimize your financial plan along with identifying the impact of potential future tax changes.

At its core, the CFP® Fast Track equips you with the expertise to offer sound financial advice, specializing in areas such as retirement planning, risk management, taxplanning, and wealth management. By pursuing this course, you become proficient in helping individuals and companies achieve their financial goals.

Tax Considerations Be mindful of tax implications related to your goals. Certain investments or strategies may offer tax advantages, while others could result in higher tax liabilities. Consulting with an advisor can help you optimize your financial plan along with identifying the impact of potential future tax changes.

I have increasingly witnessed registered investment adviser (RIA) firms, as well as brokerage firms, generally disavow (often in their client services agreement) any duty to manage the investment portfolios of…

Wealth management is an important aspect of the financial world that focuses on managing wealth to help individuals and families achieve their financial goals. Wealth management involves a range of financial services as an investment, finance, real estate, tax, and risk management.

These professionals also hold expertise in various fields, such as retirement planning, taxmanagement, estate planning, investment management, insurance, debt management, wealth management, and more. Usually, portfoliomanagers are one of two kinds: active or passive.

Dear Zoe Experts, I’ve been looking for taxplanning guidance and am deciding whether to hire a financial advisor or an accountant. Financial advisors focus primarily on investments, while accountants focus more on taxes and other record-keeping aspects of finances. You’re on the right track!

Some of the most popular ones include – PortfolioManagement Course – There are several business schools and other institutions in India offering this and similar courses and it involves the basic and advanced concepts in the financial planning and management of portfolios for clients.

Some common career paths for investment advisors include working as wealth manager, family office, portfoliomanager (PMS), Retirement Planner, Estate Planner. Investment advisors can also specialize in specific areas such as retirement planning, taxplanning, or portfoliomanagement.

This type of investing requires a portfoliomanager and often a team of analysts who alter, adjust, and move securities in real-time with the goal of a larger return. . To start, the management fees alone are often overwhelming, not to mention the added fees for buying and selling assets. Building Your Strategy.

The scope of wealth management goes beyond traditional financial planning and investment advisory services, encompassing a more holistic approach to personal finance. Wealth managers collaborate with their clients to develop customized strategies for asset allocation, taxplanning, estate planning, and risk management.

Financial advisors can handle asset allocation and portfoliomanagement, monitoring your investments for adherence to your agreed-upon investment strategy. Financial Planning: This involves creating a comprehensive financial plan, considering all aspects of your financial situation.

We have new planning software that does a much better job of delivering advice to younger clients (Elements) and to pre-retirees and retirees (Income Laboratory), new software that makes it much easier to build office workflows (Hubly), and automated client communication tools that ensure that nothing falls through the cracks (Pulse360 and Knudge).

As software automates the process of putting portfolios on the efficient frontier, and now handles the heavy lifting of harvesting tax losses and rebalancing, portfoliomanagement becomes increasingly commoditized.

These services often include recommendations on investments, financial planning, retirement, Social Security, Medicare, taxplanning, and other wealth-related topics. An hourly financial advisor is someone who provides financial advisor for a set hourly rate. Hourly financial advisors are not common. Jon Luskin. Rick Ferri.

When you have the resources to make an impact, this type of planning helps you pinpoint what you want to accomplish for your family, community, and society. Steps to Setting Up a Philanthropy Fund Taking the proper steps in the beginning can give your charitable giving plan a solid foundation.

And Wall Street didn’t work out for a variety of reasons, but I ended up working sort of an adjacent industry in the portfoliomanagement software business, and really wasn’t where my passion was. So there’s the, “Hey, I’ll work with you and we’ll develop goals and a plan how to get there.”

Also in industry news this week: A majority of married women are their family's primary financial decision-makers, according to a CFP Board study, which also identifies the sometimes-differing planning priorities of female and male clients A report from AdvisorTech firm Orion finds that while a majority of advisory firms plan to increase their tech (..)

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content