This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

But despite recognizing the impact of investment variability and sequence of return risk on a financial plan, advisors have generally ignored the same historical trends for inflation in their clients' financial plans.

But despite recognizing the impact of investment variability and sequence of return risk on a financial plan, advisors have generally ignored the same historical trends for inflation in their clients' financial plans.

Assuming that you have a financial plan with an investment strategy in place there is really nothing to do at this point. Ideally you’ve been rebalancing your portfolio along the way and your asset allocation is largely in line with your plan and your risktolerance. Focus on risk.

Monte Carlo simulations have become a central method of conducting financial planning analyses for clients and are a feature of most comprehensive financial planning software programs. a client who really wanted to guard against downward-spending-adjustment-risk might forgo income increases entirely).

The choice between stocks and bonds depends on their individual circumstances, such as risktolerance, time horizon, and financial goals. Bond Basics: How Bonds Work and Reasons to Add Bonds to Your Portfolio Stock vs bond historical returns by calendar year Investors dont hold bonds to outperform stocks over the long run.

Simple heuristics – such as planning on spending 70% of your current income or being able to spend down a fixed percentage of your portfolio annually – fall short when life gets in the way. Answers to questions surrounding “Can I retire on a million dollars?” or “Can I retire with two million dollars?”

Last year’s considerable losses and market fluctuations underscore the need for clients to assess their retirementplans to ensure it aligns with their objectives, financial situations, timelines, and attitudes toward market volatility. You can help them start the year right by conducting a retirement checkup.

Rather I suggest an investment strategy that incorporates some basic blocking and tackling: A financial plan should be the basis of your strategy. Any investment strategy that does not incorporate your goals, time horizon, and risktolerance is flawed. View all accounts as part of a total portfolio. Costs matter.

This is the time to review your portfolio allocation and rebalance if needed. For example, your plan might call for a 60% allocation to stocks but with the gains that stocks have experienced you might now be at 70% or more. Manage your portfolio with an eye towards downside risk. Click To Tweet.

If you own 10,000 shares, you receive $40,000 in dividend income (before taxes) and have a portfolio currently worth $2M. You’ll receive the same $40,000 in dividend income and the value of your portfolio drops to $1.5M. Dividend paying stocks and funds can be a great addition to a portfolio.

While grappling with various aspects of retirementplanning, it is imperative to acknowledge a critical factor that often does not receive its due attention – longevity risk. Longevity risk refers to the risk that people are living longer lifespans than previous generations.

For one person, that might mean reassessing their risktolerance and portfolio holdings to make sure that they hold assets that will at least sustain their value or provide a safer return, such as an interest rate or a dividend yield. What Can We Expect from the Markets? Why Meet with a Financial Advisor?

Ad Build a portfolio through a unique investing experience. The trust holds and manages the properties, giving you a diversified portfolio. Mutual funds are usually actively managed portfolios that attempt to outperform the market (though they seldom do). Build your portfolio alongside over a million other community members.

This is where diversifying your investment portfolio comes into play. Diversifying your investment portfolio is a vital strategy for managing risk, optimizing returns, and achieving your financial goals. However, diversifying your investment portfolio can help reduce your overall investment risk.

Investment management companies – firms that provide individual portfolio management and may work with other investment companies. For example, do you want to make investment decisions or let the experts do it through a managed portfolio? Managed investment options through Charles Schwab Intelligent Portfolios.

This advanced language processing technology has also greatly impacted the financial advisory sector, prompting a critical question: Can ChatGPT replace human financial advisors in retirementplanning? Personalized guidance, empathy, and a deep contextual understanding are integral to effective retirementplanning.

FINANCIAL PLANNING What is Portfolio Rebalancing? Investments can be risky since markets constantly fluctuate, but strategies are available to help you maintain a well-balanced portfolio. When people buy and sell sections of their portfolio to maintain a consistent asset allocation, they are rebalancing their investments.

1] What are Your Investment Goals and RiskTolerance When selecting investments for your IRA, consider your investment goals and risktolerance. Your goals may be different depending on your age, retirement timeline, and lifestyle.

When investing in a 401(k), one of the most important decisions you can make is how often to rebalance your portfolio. Rebalancing involves adjusting the mix of assets in your 401(k) portfolio to maintain a desired level of risk and return. This article will explore how often to rebalance your 401(k). Need a financial advisor?

Take Advantage of RetirementPlans and Matching Contributions. Most employer retirementplans allow you to save on a tax-deferred basis, meaning that contributions into these types of accounts are not considered in calculating your taxable income. . Determine an Appropriate RiskTolerance for a Longer Time Horizon .

Maybe Tim Cook or Jensen Huang will do stupid things in the future that hurts their stocks but the risk that their behavior blows up those stocks isn't really on the table. I also owned the name for a couple of more risktolerant clients. I've never owned one of the shipping stock companies but the space always intrigued me.

Rebalancing your 401(k) and investment portfolio is an important part of a successful investment strategy. Your asset allocation is the percentage of your portfolio that you distribute between different asset classes, like stocks and bonds. Why do you need to rebalance your portfolio? Why does this matter?

Then you can choose the options that are best for you when you create your investment portfolio and financial plan. The benefit of using a Robo-advisor is that the fees are typically lower, even though you are getting customized portfolio recommendations. Prepare with your risktolerance in mind.

While they do share some similarities, there are enough distinct differences between the two where they can just as easily qualify as completely separate and distinct retirementplans. Either plan is an excellent choice, particularly if you’re not covered by an employer-sponsored retirementplan. Not exactly.

The stock market has returned an average of between 9% and 11% over the past 90 years and that’s the kind of growth that you’ll need to tap into if you want to retire at 50. Your retirementplan shouldn’t be. Get in touch with an Independent Financial Professional to see if you're on track to meet your retirement goals.

Your financial goals and risktolerance are the roadmap for your entire wealth management strategy, shaping your decisions and the services you require. Long-term goals typically encompass retirementplanning, wealth preservation and estate planning.

This data can serve as a baseline for tailoring your retirementplan, taking into account factors such as inflation, your current age, and your desired retirement age. One of the fundamental principles of retirementplanning is to resist the temptation of premature fund withdrawal, especially in response to market fluctuations.

These professionals meticulously assess your financial situation, income level, and retirement goals to tailor personalized strategies. For instance, they can guide you on leveraging employer-sponsored retirementplans, such as a 401(k) with employer matches, to optimize your contributions and harness the full benefits of the accounts.

Invest in the Stock Market Suggested Allocation: 40% to 50% Risk Level: Varies Investing Goal: Long-term growth The stock market is where most of us save for retirement already, mostly through the use of tax-advantaged retirementplans, like a 401(k), SEP IRA, or Solo 401(k).

And how does it compare to the 401k and other retirementplans that exist? Being a self-employed retirementplan , the SIMPLE IRA gives you the discretion of what exactly you want your money invested into. . Most retirementplans — 401(k)s, regular IRAs, or Roth IRAs, etc. What is a Simple IRA?

Pam and I discussed how a successful multi-family office operates, the profile of clients, how her firm charges for its services, the mindset advisors need to work with wealthy (and oftentimes famous) individuals, where alternatives fit in her clients’ portfolios, and the role that technology plays in delivering exceptional service.

Then you can choose the options that are best for you when you create your investment portfolio and financial plan. The benefit of using a robo-advisor is that the fees are typically low, even though you are getting customized portfolio recommendations. It is a great way to get started with building wealth with little money.

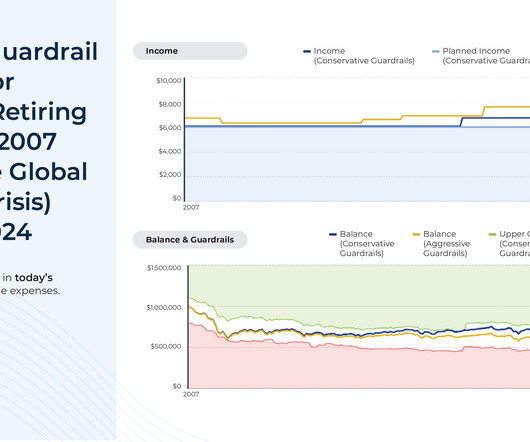

For people nearing retirement, these challenges can be even more daunting. A market downturn at the start of retirement, hitting portfolio values when retirees begin to take account withdrawals, can be unsettling, even for seasoned investors. Many near-retirees see their highest portfolio values just before retirement.

Plan wisely for your retirement. Retirementplanning is essential for everyone, but it is especially crucial if you manage your finances independently. So, if you decide on DIY financial planning, devise strategies to save and invest money for your retirement.

Your financial goals and risktolerance are the roadmap for your entire wealth management strategy, shaping your decisions and the services you require. Long-term goals typically encompass retirementplanning, wealth preservation and estate planning.

They can provide guidance and advice on investing, retirementplanning, tax optimization, and more. Time-saving: Financial planning can be time-consuming, but by hiring a financial advisor , you can save time and energy, knowing that an expert is taking care of your finances.

Starting early with investing for retirement is so important to secure your future self. This means that saving for retirement should be a component of your overall financial portfolio and wealth-building strategy. So, let’s discuss how to save for retirement in your 20s! The 401(k) Plan 2. Traditional IRA 3.

One thing that I have craved for investors is a tool that allows you to sync all your financial accounts – your investment portfolio, checking and savings accounts, credit cards and other loan accounts – in one place, and then provides an investment-related analysis of your entire portfolio.

According to the Department of Labor , “Based on the experience of Council members, and testimony and conversations with recordkeepers, the value of uncashed retirementplan checks likely exceeds $100 million per year but could be considerably larger.

Discretionary expenses include money spent traveling, eating out, contributing to savings and retirementplans or occasional purchases and upgrades. Maximize Your RetirementPlan Savings . Employers often match a portion of this contribution to a retirementplan as an employer benefit.

The answer lies in smart and strategic retirementplanning. Gone are the days when retiring at 60 was a one-size-fits-all goal. It’s time to rethink when to start stashing away those savings and how to modify your plan in a world that’s constantly changing.

However, engaging in open and insightful conversations with your financial advisor is important to ensure you understand your portfolio well and can make informed decisions. Having a proactive approach can help you navigate the intricacies of investing and have a deeper understanding of your portfolio.

For example, an employer-sponsored 401(k) or 403(b) retirementplan is a wonderful perk. You may approach your plan administrator to convince them to add options that promote gender equity to your retirementplan. The Envision Wealth Planning investment process starts with qualifying and quantifying your goals.

Blind spots in retirementplanning are those aspects that are often overlooked, either intentionally or subconsciously. From seemingly harmless low-interest debt to underestimating the emotional impact of transitioning out of the workforce, various factors can disrupt your peace of mind during your retirement years.

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content