This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

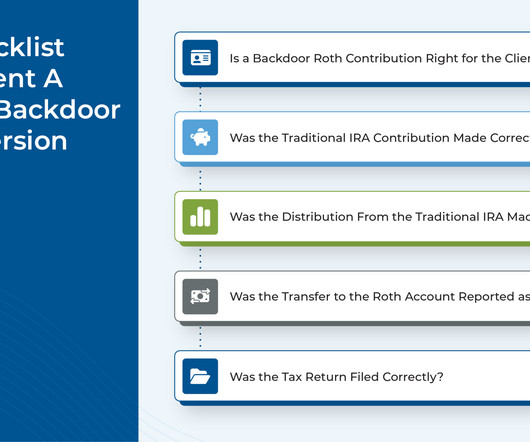

There are many taxplanning strategies that allow financial advisors to demonstrate the ongoing value they provide to clients in exchange for the fees they charge. Part of this value is understanding the detailed nuances that make a strategy effective and implementing it correctly, avoiding issues with the IRS down the line.

Taxplanning might not top everyone’s list of leisure activities, but in the middle of tax season, theres a hidden opportunity. In this episode, we talk about five strategies you can use during tax season to create opportunities to help you reach your financial goals.

The start of a new year presents opportunities for clients to make positive changes for their financial futures. According to a recent Advisor Authority survey, powered by the Nationwide Retirement Institute®, only 20% of non-retired investors have confidence in their retirementplans despite market volatility.

Anyone who owns company stock will eventually have to decide how to distribute their assets — typically when there is a job change or retirement involved. You cannot sell the securities within the retirementplan, then move cash to a brokerage account and purchase the same shares at that point. This would negate the NUA benefit.

What are appropriate checklists for year-end taxplanning? Tax planners often develop checklists to guide taxpayers toward year-end strategies that might help reduce taxes. Certain tax benefits may be available if you can claim an individual as a dependent. Family taxplanning. Financial investments.

This is the time to do comprehensive financial planning: retirementplanning, investment planning, taxplanning and estate planning. Help her focus on immediate needs, pay bills, monitor cash flow and review her investment portfolio.

Total 401(k) contribution limits: Including employer matches, after-tax contributions, and other contributions, the total limit is $69,000 (or $76,500 for individuals aged 50 and above). The key difference lies in the final destination of the after-tax contributions.

According to the Department of Labor , “Based on the experience of Council members, and testimony and conversations with recordkeepers, the value of uncashed retirementplan checks likely exceeds $100 million per year but could be considerably larger.

He is a BFSI Industry Veteran with over 30 Years of Experience across various functions Financial planning is, in the words of renowned author Alan Lakein, “Bringing the future into the present so that you may do something about it now.” It also guides on building a client base and becoming a successful financial planner.

If you are planning your career in this direction, it is the right time to take the plunge in this trade. Whether you are starting up your career in this trade or looking for a mid-career switch this career option presents to you immense growth opportunities. Types of Investment Advisor Courses and Training Programs.

One major thing to consider when doing so is the tax bill that may come along with it. The good news is you may be able to take advantage of a little-known tax break called net unrealized appreciation (NUA) — if you qualify. . What Is NUA? The employer stock is distributed in-kind and is usually moved to a brokerage account.

Retirementplanning can be a bit complex. There are multiple factors to weigh in, right from healthcare and inflation to estate planning, business succession planning, taxplanning, and more. However, the main drawback to this can be the lack of foresight regarding what and how to plan.

Retirementplanning is a must, so start with maximizing your 401k and Individual Retirement Accounts (IRAs). Additionally, both partners should think of the future as much as they do about the present. Consider planning your expenses as a couple: Earning couples have more disposable income than others. To conclude.

Aaron Parish [link] Level Wealth Stephan Shipe Home Scholar Advising Ohio Curtis Bailey quietwealth.net Flat Fee of $6,000 per year charged at $500 per month Brian Tegtmeyer Home Flat Fee financial planning, investment management, and taxplanning for new retirees. I also provide one-time retirementplans for DIY investors.

Investments, taxplanning, retirementplanning is a dynamic field. The best strategies employed a few years back might not be the best for the present and the future. In simple words, you must have fire in your belly and without it, you’d never succeed in this race. A Person Who Is Always Curious.

These professionals meticulously assess your financial situation, income level, and retirement goals to tailor personalized strategies. For instance, they can guide you on leveraging employer-sponsored retirementplans, such as a 401(k) with employer matches, to optimize your contributions and harness the full benefits of the accounts.

As we reposition portfolios, there is an opportunity to harvest losses in taxable portfolios that exceed the value of any realized gains for this tax year, and a meaningful market decline allows us to “bank” losses to be used in future years if and when markets recover. FINANCIAL PLANNING Home Refinance. Financial Plans.

It is hard to feel confident about the market’s eventual recovery when we are in the midst of a sharp decline, but the market’s history is a continual cycle of ups and downs, and we believe that the current downturn presents some positive opportunities to take steps that are consistent with your overall plan, while minimizing tax consequences.

Of course, individuals over age 50 are usually entering their highest earning years, so no longer being able to exclude $7,500+ from income will end up costing most high earners in the form of higher taxes for the year. that presents significant hurdles for small employers. it’s clear that investors need to be adaptive in taxplanning.

Instead of just talking about taxes in retirement, Joe presents a clear problem (overpaying taxes) and an actionable solution (his free video series on taxplanning through retirement). A strong hook: He immediately addresses a common pain point: Worried about taxes eroding your retirement savings?

There now exists a meaningful incentive for many long-time Intel employees to retire from Intel before May 2021. We’ve received many questions so far about the relevance and magnitude of these changes on one’s retirementplans. What is Changing With Intel’s Minimum Pension Plan.

2023 may see several changes with respect to retirementplans, Social Security, etc., under the Securing a Strong Retirement Act of 2022 (SECURE 2.0). However, these investments do present a high risk, which is why it is essential to be careful and understand their underlying cons before investing.

This article will go over the fundamentals of the Roth IRA retirement account, how not paying taxes on a Roth IRA can help you save money in retirement, and ways to use the account to unlock its tax benefits. If you are saving for retirement, you would have likely come across or heard of an IRA. What is a Roth IRA?

They’re well-versed in recommending vital products like life insurance and are wizards at taxplanning. Presenting with Panache: Your voice matters. A Spectrum of Opportunities The canvas of financial advisory is vast and varied: Delve into niches like retirementplanning or wealth management.

The field of investment advisory presents a world of opportunities for individuals passionate about finance and investments. Some common career paths for investment advisors include working as wealth manager, family office, portfolio manager (PMS), Retirement Planner, Estate Planner.

Some years back, as a standard part of my industry presentations, I would ask the audience how many of them would, if they could, go back to where they were 10 or 15 years ago, career-wise or, for that matter, life-wise. . Very rarely would a hand go up.

(Click here for Blog Archive)(Click here for Blog Index) (Presentations in this Blog were created using the InsMark Loan-Based Split Dollar System) Editor’s Note: This blog presents a sizzling loan-based split-dollar plan. This executive benefit will be difficult to justify if interest rates increase considerably.

Make the best use of tax-saving strategies. Taxplanning should form the crux of your financial planning. Remember, individuals and businesses are subject to different tax codes. For instance, entrepreneurs and business owners are entitled to several tax-saving schemes that do not apply to non-entrepreneurs.

Below are five benefits of working with a financial advisor and how they can help you retire with more wealth: 1. They help you optimize taxplanningTaxplanning is an important aspect of financial planning that can significantly impact your long-term wealth accumulation.

(Click here for Blog Archive)(Click here for Blog Index) (Presentations in this Blog were created using the Loan-Based Split-dollar System and Wealthy and Wise®) Blog #221 follows up on Blog #220, which described coupling Premium Financing with Wealthy and Wise® to produce a powerful wealth planning concept called “Zero Estate Tax.”

(Click here for Blog Archive)(Click here for Blog Index) (Presentations in this blog were created using the InsMark® Illustration System) Reasons to Act Now You should acquire your life insurance as soon as you determine its usefulness.

(Click here for Blog Archive)(Click here for Blog Index) (Presentations in this blog were created using the InsMark® Illustration System) Other than the principal owners, who are the key executives of any business? What are the benefit plans […]. Minority-owner executives. These are often the firm’s key personnel.

(Click here for Blog Archive)(Click here for Blog Index) (Presentations in this Blog were created using InsMark’s Wealthy and Wise® Advanced System.) estate planning has escaped the tax bombs Democrats wanted to drop. It looks like U.S.

(Click here for Blog Archive)(Click here for Blog Index) (Presentations in this blog were created using the Premium Financing System and Wealthy and Wise® ) This Blog describes combining our Premium Financing and Wealthy and Wise® Systems to produce a powerful wealth planning concept called “Zero Estate Tax,” Most clients prefer comparing their (..)

The affluent also understand the importance of minimizing taxes on their investment gains and employ sophisticated taxplanning strategies to take advantage of tax-efficient investment vehicles and maximize their after-tax returns. This can be a tax-efficient vehicle for retirementplanning and wealth transfer.

Hence, it becomes essential to follow a rational financial plan that focuses on your short and long-term financial goals and ensures financial security not just in the present but also in the future. Not creating a comprehensive financial plan Financial planning for physicians and healthcare professionals is essential.

If you are a high-net-worth individual and wish to learn about wealth preservation, tax-saving strategies, and management of large estates; engage the services of a wealth advisor who can advise you on the same. Keep reading to know more about the financial planning process for high-net-worth individuals and how it can benefit you: 1.

The professional restrictions that resulted from COVID-19 may have passed, however, remote work has remained an ever-present feature of the post-pandemic employment arena. With over 22 million Americans working remotely , understanding the tax deductions available for home offices is more relevant than ever.

Strategic taxplanning for PCPs involves the optimal use of tax-advantaged accounts. Health Savings Accounts (HSAs) offer tax-deductible contributions, tax-free growth, and withdrawals for medical expenses. While QBI deductions may soon be unavailable, other deduction options remain.

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content