This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

To start, Taylor refined his ideal client profile to focus on those he could best serve: diligent savers over age 50 with a retirement nest egg between $2M and $10M. These clients, typically in or near retirement, face key challenges like reducing taxes, managing investment risk, and maximizing income.

Let’s delve into a case in point of Coase’s theorem: If you wanted to peddle the narrative that government spending is out of control, you might present a chart like the one above, which is an exact replica of a chart that appeared recently in a piece of research from a major Wall St. investment firm.

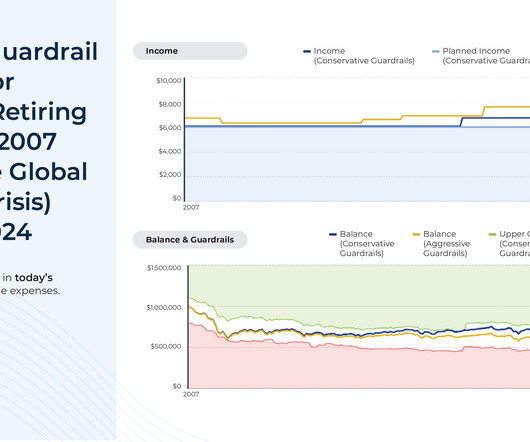

And when it comes to retirement planning, one popular technique is the use of ‘guardrails’, which set an initial monthly withdrawal rate that can be later adjusted as the size of the client’s portfolio changes. Financial advisors have a wide range of strategies at their disposal to create financial plans for their clients.

(monevator.com) Retirement accounts Half of American workers now have a 401(k) account. wsj.com) On the downside of tax-deferred retirement accounts. morningstar.com) Wealth Tony Isola, "Wealth creation is about delaying and compounding present pleasures into the future, not constant stimulation and engagement."

morningstar.com) Christine Benz and Jeff Ptak talk with Mike Moran, managing director and pension strategist for Goldman Sachs ($GS) about the state of retirement preparedness. nytimes.com) Retirement Some alternatives to a fixed retirement withdrawal rates. thinkadvisor.com) What makes up the three-legged stool of retirement.

Over time, advisors shifted toward more analytical approaches, such as investment management and retirement planning. Typically, these values fall into 2 categories: realized values, which are already present in a client's life, and aspirational values, which represent qualities they want to embody.

First, I would ask clients how much they were saving each year for retirement. They knew what they were putting directly into their retirement accounts, but I wanted to know how much of their income they were saving for the future. Then I would present the plan to the client.

thomaskopelman.com) Who is eligible for the retirement savings tax credit? contessacapitaladvisors.com) Why it pays to get certain expenses out of the way before retirement. tonyisola.com) "Personal Finance Mistakes You're Probably Making" a presentation by Prof. podcasts.apple.com) Morgan Housel on the 'art of spending money.'

investmentnews.com) Retirement It's inevitable we will see more older workers. klementoninvesting.substack.com) The reasons why people un-retire. riaintel.com) Why you should flip your plan presentation meetings on their head. (financial-planning.com) Wealth.com's Ester will help you read estate planning documents.

Also in industry news this week: The SEC this week announced a proposed rule that would require RIAs to collect and verify their clients' personal information in an effort to prevent illicit activity, though many firms likely are taking many of these steps already Why larger RIAs and those that have been acquired tend to have worse client and staff (..)

Enjoy the current installment of "Weekend Reading For Financial Planners" - this week's edition kicks off with the news that the Department of Labor this week released its long-awaited "retirement security rule", its latest effort to curb conflicts of interest around retirement savings recommendations.

Owners tend to be fairly well off, and each incremental dollar they earn is more likely to be spent elsewhere – retirement savings, durable goods, etc. We present the first causal analysis of recent large minimum wage increases, focusing on 47 larger U.S. It has aa much smaller impact on the local economy.

Also in industry news this week: Edward Jones, which added more new CFP professionals than any other firm last year, announced that it is planning to offer financial planning services nationwide, highlighting the value for RIAs and other firms of differentiating themselves amidst increased competition not only for clients, but also for advisor talent (..)

Enjoy the current installment of “Weekend Reading For Financial Planners” - this week’s edition kicks off with the news that while banks have been able to attract a younger and more diverse set of financial advisors compared to the rest of the industry, thanks in part to their built-in referral stream, a relative lack of independence (..)

”, a series of measures that will have significant impacts on the world of retirement planning. How the holiday season presents an opportunity to have important money-related conversations with family members. How ‘regifting’ can help save money and reduce waste.

By distilling hundreds of pieces of information into a single number that purports to show the percentage chance that a portfolio will not be depleted over the course of a client's life, advisors often place special emphasis on this data point when they present a financial plan.

AUM detractors like Sethi often present a calculation that compares the performance of 2 identical portfolios – one managed by an advisor who charges a 1% AUM fee for 20+ years, and one without an advisor – illustrating how the fee can significantly erode the cumulative value of their portfolio by the time they reach retirement.

By distilling hundreds of pieces of information into a single number that purports to show the percentage chance that a portfolio will not be depleted over the course of a client’s life, advisors often use this data point as the centerpiece when they present a financial plan.

Early retirement has become a popular financial goal. Even if you never retire early, just knowing that you can is liberating! Can You Really Retire at 50? Can You Really Retire at 50? Table of Contents Can You Really Retire at 50? FAQs on Retiring Early at 50 It’s a big bold claim – retire at 50?

Realistic Retirement Planning My children have consistently (and kindly) remarked about how grateful they are to have been able to graduate (with honors) from fine universities without any debt. Our retirement planning took a hit to do so. Thanks for reading. However, achieving that goal came at a cost.

abnormalreturns.com) Comparisons Ramp, "Ultimately, what holds true value in life is being present for your friends and family in their time of need, rather than relinquishing your integrity for the sake of money or material possessions." whitecoatinvestor.com) The key to retirement withdrawals is flexibility.

And for those who don't want to join the team full-time but would simply like to 'Nerd Out' with us for a bit and share what they do or know with their fellow advicers, remember to check out our "How To Contribute" page to see how you can engage with the Kitces platform as a guest writer, presenter, or podcast guest!

Now this begs the question If your late-stage private company presents a tender offer, whats the right move to make for your immediate and long-term financial well-being? Lets assume your company announces tomorrow that a tender offer is being presented to all employees with shares of company stock. Schedule an introductory call today.

Now that you’ve worked to set up a great life after working for so long, it can be a great idea to help avoid those retirement blues and start your retirement off with a bang! One way to kick things off the right way is to consider having a party with your friends and family to celebrate your retirement. Throw a Party!

Historically, advisors haven't had many avenues to manage clients' 401(k) plan accounts, since unlike traditional custodial investment accounts, advisors generally lack discretionary trading authority in employer-sponsored retirement plans.

Historically, advisors haven't had many avenues to manage clients' 401(k) plan accounts, since unlike traditional custodial investment accounts, advisors generally lack discretionary trading authority in employer-sponsored retirement plans.

Whether they are on the cusp of retirement or living as a retiree, this is an impactful time of transition. Navigating the Retirement Transition with “Switches” Because the transition to retirement is dynamic and requires financial, lifestyle, and social choices, clients need a full understanding of their “switches” or options.

Enjoy the current installment of “Weekend Reading For Financial Planners” - this week’s edition kicks off with the news that a Federal district court in Texas has put a stay on the effective date of the Department of Labor’s (DoL’s) new Retirement Security Rule (aka “Fiduciary Rule 2.0”),

and why Suzanne has taken an approach of not trying to work and save for retirement as a time to enjoy when she gets there, but instead has structured her busy-season-light-season approach to client meetings to allow for more space to enjoy trips and time with her family now, instead.

Enjoy the current installment of “Weekend Reading For Financial Planners” - this week’s edition kicks off with the news that a Federal district court in Texas has put a stay on the effective date of the Department of Labor’s (DoL’s) new Retirement Security Rule (aka “Fiduciary Rule 2.0”),

Before your generation, retirement had long been perceived as a time when life took a downward turn. Baby Boomers have been cool kids since their inception: introducing rock n roll, pop culture, mainstream technology, and now, reshaping retirement into a time of exploration, passion, and learning. Keeping Money for Retirement.

Retirement is a time for rest, relaxation, and a chance to sit back and appreciate all that we have gained. However, it’s important to recognize that financial stability is crucial for personal growth during retirement. Retirement is also a time for reflection and personal growth.

Retirement planning can be a bit complex. Given the complexity and magnitude of things necessary for a comfortable retirement, starting planning from a young age is also essential. At the age of 30, your daily expenses can significantly differ from what you would need in retirement. Ten retirement expenses to keep in mind: 1.

At 50 though, you do need to have some context for how viable your idea of retirement is. My reasoning is as it has always been, my income is levered to the ups and downs of the stock market, I don't ever want to retire, we have been living below our means for ages and now all the more so having just paid off our mortgage.

When financial professionals know how to effectively present a financial plan, they can better engage clients in the planning process and earn clients for life. Presenting a financial plan, however, isn’t as simple as running through the numbers. Communicate Clearly and Effectively. Divide and Conquer. Sometimes less is more!

The hope is that these conversations will help the prospect ease into a positive frame of mind (by thinking about a vacation, retirement, or another future aspiration) and, at the same time, present the advisor with an opportunity to show how their services can help the prospect achieve their goals.

Starting early with investing for retirement is so important to secure your future self. This means that saving for retirement should be a component of your overall financial portfolio and wealth-building strategy. So, let’s discuss how to save for retirement in your 20s! How do I start putting money away for retirement?

There’s a great scene in Midnight in Paris about nostalgia that I think about a lot: Some people always think the past is better than the present because of this golden age line of thinking. I always see memes like this going around Twitter: Life would be better is this was true. Unfortunately, it’s not (see here and here).

by Jake Anderson, Paraplanner Retirement accounts like 401(k)s and IRAs allow individuals to save for their future in a tax advantaged manner. This gives you ample time to grow your savings and investments for retirement. IRAs and 401(k)s are primarily designed to help fund retirement not pass wealth onto future generations.

Whether planning for retirement, investing in volatile markets, or managing tax implications, clients are often presented with intricate information that can leave them overwhelmed, confused, and anxious, undermining their ability to make informed decisions.

What's unique about Jennifer, though, is how, after more than a decade of building her own successful solo practice, she intentionally decided to merge her practice with another solo practitioner when an unusual crisis opportunity presented itself, and handle the more complex business management dynamics that followed, so that she could fulfill her (..)

A much-anticipated feature of this edition is the annual indexed retirement and Social Security numbers for 2025, conveniently presented in an easy-to-reference table. The J anuary issue of the Journal of Financial Service Professionals has arrived, and its a must-read for anyone in the financial services community.

What's unique about Jeff, though, is how he built his own financial planning spreadsheets in Excel, and has developed coding and integrations that automatically populate into a PowerPoint presentation, that he then shows clients to help build a story for their financial plans and give them the motivation they need to achieve their financial goals… (..)

If you are an art lover and want to build your own collection in retirement, here are small steps to get you started: Art Demands You Listen to Your Heart. Plus, some of the fun of adding a new piece to your collection is figuring out how to best present it! 1] [link]. [2] 2] [link]. [3] 3] [link]. 1] [link]. [2] 2] [link]. [3]

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content