This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Taxes are a central component of financial planning. Almost every financial planning issue – whether it is retirement, investments, cash flow, insurance, or estate planning – has tax considerations, and advisors provide a great deal of value in helping clients minimize their overall tax burden.

Taxplanning might not top everyone’s list of leisure activities, but in the middle of tax season, theres a hidden opportunity. In this episode, we talk about five strategies you can use during tax season to create opportunities to help you reach your financial goals.

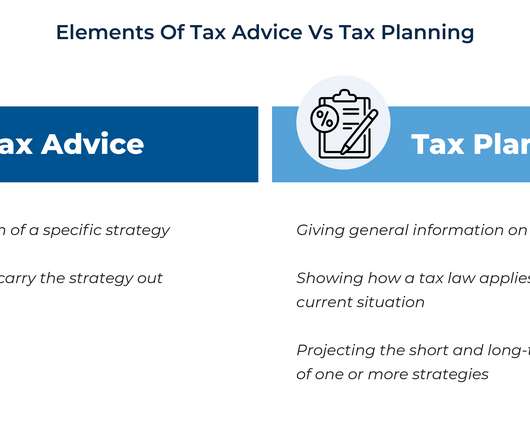

There are many taxplanning strategies that allow financial advisors to demonstrate the ongoing value they provide to clients in exchange for the fees they charge. Part of this value is understanding the detailed nuances that make a strategy effective and implementing it correctly, avoiding issues with the IRS down the line.

Retirementplanning can be a bit complex. There are multiple factors to weigh in, right from healthcare and inflation to estate planning, business succession planning, taxplanning, and more. However, the main drawback to this can be the lack of foresight regarding what and how to plan.

The start of a new year presents opportunities for clients to make positive changes for their financial futures. According to a recent Advisor Authority survey, powered by the Nationwide Retirement Institute®, only 20% of non-retired investors have confidence in their retirementplans despite market volatility.

What are appropriate checklists for year-end taxplanning? Tax planners often develop checklists to guide taxpayers toward year-end strategies that might help reduce taxes. Certain tax benefits may be available if you can claim an individual as a dependent. Family taxplanning. Financial investments.

Anyone who owns company stock will eventually have to decide how to distribute their assets — typically when there is a job change or retirement involved. Distributions only qualify for NUA treatment if completed after the triggering event (separation from service, reaching retirement, death or disability). Cost Tradeoff.

The reality for those with various employers is that untracked retirement savings might lead to missed financial growth opportunities and instability. Diligent oversight and management of these retirement accounts is essential for anyone aiming to build a solid financial foundation for a comfortable and secure retirement.

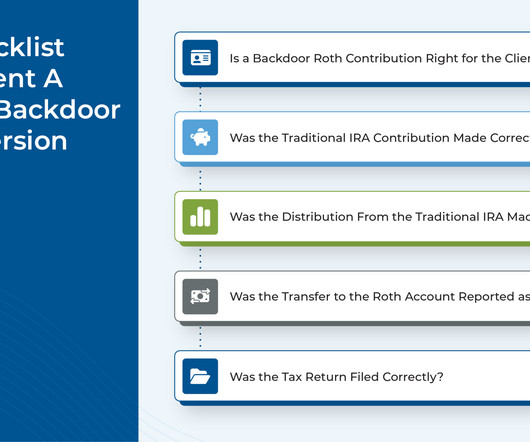

Backdoor strategies are retirement contribution methods that allow individuals to bypass income limits and contribute to tax-advantaged retirement accounts. The strategies typically involve making after-tax contributions to a traditional IRA or 401(k), then converting those funds into a Roth IRA or Roth 401(k).

This is the time to do comprehensive financial planning: retirementplanning, investment planning, taxplanning and estate planning. Help her focus on immediate needs, pay bills, monitor cash flow and review her investment portfolio.

According to a survey, a significant majority of Americans, approximately 80%, share the common notion that the point of working hard in your adult life is so you can enjoy a nice retirement. After years of dedicated labor and hard work, the prospect of a peaceful retirement appeals to everyone.

For those employees eligible for Intel’s minimum pension benefit (MPP) at retirement, the interest rate used to calculate today’s value of that benefit is changing. This means that your estimated Minimum Pension Plan benefit amount is significantly reduced or erased altogether in many cases. What should I do next?

When tax rates are stable, it’s wise for you to defer as much income as possible from one year to a later year and to accelerate deductions so that you can postpone payment of the tax. When you eventually realize the income at some future point, it’s possible that you’ll be retired and/or in a lower tax bracket.

Navigating the complex world of personal finance, especially with retirement looming on the horizon, can be daunting. Working with a financial advisor can significantly enhance your chances of retiring with more wealth. Hiring the best financial advisors for retirement can lead to better savings and investment outcomes.

However, a period of lower income in 2024 could present valuable taxplanning opportunities. One potential benefit of a job layoff is a temporary drop in your federal income tax bracket, which can create opportunities for future tax savings.

I have to tell them there’s a small chance of that happening, but an easier route would be to buy a boring business from someone who’s retiring. Then we do the financial plan and taxplanning around that—it’s been a lot of fun. This is an easier way to get the lifestyle you want.

Retirementplanning is a must, so start with maximizing your 401k and Individual Retirement Accounts (IRAs). Additionally, both partners should think of the future as much as they do about the present. Consider planning your expenses as a couple: Earning couples have more disposable income than others. To conclude.

From quarterly estimated taxplanning to equity compensation and crypto taxplanning, diversifying your service offerings can not only set you apart from the competition, it can also help you significantly grow your revenue and retain clients.

While these can be avoided, there is another cash outflow that can considerably lower your savings and returns and is also hard to avoid – tax. Taxplanning is essential. Tax is charged on every penny you earn. Tax evasion is a crime, and missing tax payments can lead to legal hassles that can be hard to get out of.

Instead of just talking about taxes in retirement, Joe presents a clear problem (overpaying taxes) and an actionable solution (his free video series on taxplanning through retirement). A strong hook: He immediately addresses a common pain point: Worried about taxes eroding your retirement savings?

Here are the top five Roth-related retirement changes following the passing of Secure Act 2.0. 529 plan to Roth IRA rollovers. that presents significant hurdles for small employers. The Act stipulates that unless a plan allows catch-up contributions in Roth accounts, then no one in the plan can make catch-up contributions.

Anyone who owns company stock will eventually have to decide how to distribute those assets when leaving the company or entering retirement. One major thing to consider when doing so is the tax bill that may come along with it. For example, you retire with 1,000 shares of the company’s stock. What Is NUA? NUA Requirements.

Matthew Etzler [link] Colorado Skip Fleming Home Advice only planner Downshift Financial Home Eric Courage Margin Flat fee advisor Delaware Sam Lewis www.wecanplanforthat.com Flat Fee and hourly Advice-only only planning to help young professionals and pre-retirees retire early. Tax preparation is also available.

He is a BFSI Industry Veteran with over 30 Years of Experience across various functions Financial planning is, in the words of renowned author Alan Lakein, “Bringing the future into the present so that you may do something about it now.” It also guides on building a client base and becoming a successful financial planner.

Financial planning ensures you have adequate financial resources to achieve your life goals, such as purchasing a home, beginning a family, or retiring comfortably. Starting financial planning early in one’s career is essential, as it allows more time for savings and investments to grow.

If you are planning your career in this direction, it is the right time to take the plunge in this trade. Whether you are starting up your career in this trade or looking for a mid-career switch this career option presents to you immense growth opportunities. Types of Investment Advisor Courses and Training Programs.

Some clients opt for more aggressive gifting strategies, especially with the sunset of estate tax exemptions looming, which allows them to utilize their lifetime gift exemptions effectively. Inheritance TaxPlanning Inheritance taxes, including estate and gift taxes, are pivotal in estate planning discussions.

These numbers show an opportunity for tax practices to build deeper, meaningful relationships with their clients, helping them to navigate some of life’s most challenging financial decisions. And you’ll see in our Q&A below, that tax advisors can bring estate planning into the conversation early on in a client relationship.

Unfortunately, it could also lead to larger capital gains and taxes in the future. While there may be some truth to that, it assumes consistent investment growth and accurate predictions of future capital gains tax rates. In short, the present value of current tax savings is seen as more valuable than uncertain future tax liabilities.

A financial plan looks at your assets and liabilities, short-term and long-term needs, as well as your goals to structure your finances in a way that suits you. Want to retire early? Financial planning shatters many allusions you might have about how money works. TaxPlanning. Emotional Investment Choices.

The steps you should take if you’re retiring from Intel. What Issues Should I Consider Before I Retire? A pension (also called a Defined Benefit plan) is a promise, funded by your employer, to provide a certain monthly income to you in retirement. Intel’s pension plan is a minimum benefit pension plan.

Moreover, since they do not earn any income from their real estate investments, they may struggle to pursue other financial goals, such as retirement, higher education costs for a child, etc. High-net-worth individuals are adept at using legal mechanisms to optimize their taxplanning.

Apart from financial planning in the business sphere, entrepreneurs also need to engage in financial planning to save for retirement and financially protect their families. It is paramount for entrepreneurs to create a foolproof financial plan, not just for their businesses but also for their personal finances.

Investments, taxplanning, retirementplanning is a dynamic field. The best strategies employed a few years back might not be the best for the present and the future. In simple words, you must have fire in your belly and without it, you’d never succeed in this race. A Person Who Is Always Curious.

With reliable expertise, physicians can make informed decisions, allocate their resources strategically, and plan for significant life milestones. A well-structured plan not only serves as a roadmap for the present but also paves the way for a more secure future. A higher income does not only lead to more spending.

The new Regulations generally clarify (1) the trust look-through rules that apply when a trust is designated as a beneficiary of qualified plans (401(k), 403(b), and 457 plans generally), or individual retirement accounts, and (2) the required minimum distribution (RMD) requirements on designated beneficiaries subject to the new 10-year payout rule.

2023 may see several changes with respect to retirementplans, Social Security, etc., under the Securing a Strong Retirement Act of 2022 (SECURE 2.0). Financial goals and circumstances can change significantly over time due to events such as marriage, divorce, the birth of children, job changes, and retirement.

With its unique benefits and long-term growth potential, the Roth Individual Retirement Account (IRA) has become a popular choice among individuals seeking to build a retirement nest egg. The Roth IRA can be a reliable and tax-efficient way to save for your future. You do not pay taxes until you withdraw the money in retirement.

As we reposition portfolios, there is an opportunity to harvest losses in taxable portfolios that exceed the value of any realized gains for this tax year, and a meaningful market decline allows us to “bank” losses to be used in future years if and when markets recover. FINANCIAL PLANNING Home Refinance. Financial Plans.

It is hard to feel confident about the market’s eventual recovery when we are in the midst of a sharp decline, but the market’s history is a continual cycle of ups and downs, and we believe that the current downturn presents some positive opportunities to take steps that are consistent with your overall plan, while minimizing tax consequences.

Crafting Your Personalized Financial Plan: A Step-by-Step Guide The Role of a Wealth Manager or Financial Planner Harness Wealth Can Help What is a Financial Plan? While it may seem like a luxury that is only available to the wealthy, anyone is capable of building an effective financial plan and putting it into action.

Or maybe they began their financial planning journey because of one specific need—like saving for college or retirement. By offering holistic planning, you have the opportunity to roll all of that together to provide clients with a plan that addresses so much more.

Their wisdom extends to suggesting tax-efficient avenues for pivotal life moments, be it education or the golden years of retirement. They’re well-versed in recommending vital products like life insurance and are wizards at taxplanning. Presenting with Panache: Your voice matters. Where Do They Shine?

The field of investment advisory presents a world of opportunities for individuals passionate about finance and investments. Some common career paths for investment advisors include working as wealth manager, family office, portfolio manager (PMS), Retirement Planner, Estate Planner.

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content