This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

And the consequences for incorrect tax advice can include legal and financial penalties if a client were to be harmed by the wrong advice – which is often not covered by the firm’s E&O insurance –creating an expensive liability when tax advice goes wrong.

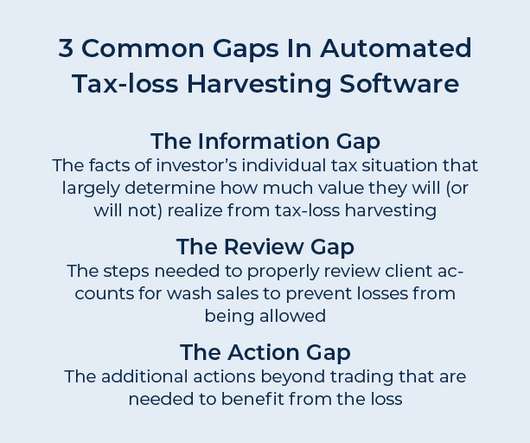

Unfortunately, much of the technology dedicated to automated tax-loss harvesting fails to consider the individual tax circumstances that drive most of the true value of harvesting losses, and instead focuses on the portfolio-management aspect of efficiently capturing as many losses as possible. Read More.

is the projected future direction of medical care, where, instead of taking a reactive approach to disease and illness, healthcare practitioners instead invest more energy focusing on preventing illness and maintaining good health in the first place through more personalized plans for patients. Specifically, Financial Advice 3.0

Financial planning and taxplanning go hand in hand. Including taxplanning as part of your service provides clients a comprehensive view of their finances and helps them achieve their financial goals. Start with Document Sharing The first step is to ask your clients to share their tax documents with you.

Finally, the annual T3/Inside Information Software Survey, which assesses the software programs used by financial advisors, found that taxplanning tools are on the rise – with adoption rates jumping from 30% to 43%.

The key point, however, is that – like many taxplanning strategies – tax-loss harvesting requires at least some individual attention to each client’s tax situation to ensure it is the right strategy for that client. With these three tools (i.e.,

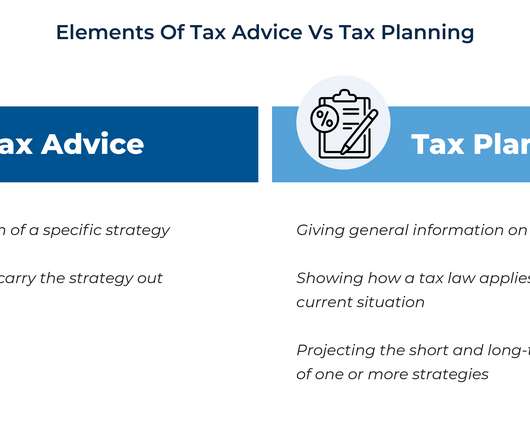

There are many taxplanning strategies that allow financial advisors to demonstrate the ongoing value they provide to clients in exchange for the fees they charge. Part of this value is understanding the detailed nuances that make a strategy effective and implementing it correctly, avoiding issues with the IRS down the line.

Advisors who can help their clients with taxplanning strategies to take advantage of PTETs – starting with determining when it’s really worthwhile to do so – can provide significant value given the complexity of the decision.

For instance, the Heath Walters Institute offers on-demand taxplanning and support for financial advisors who want to better serve their high-net-worth clientele.

Tax season is upon us, but you can start 2024 off on the right foot with taxplanning tips and strategies presented by Mike Valenti, Director, TaxPlanning and Tom Fridrich , Carson Group Manager & Sr.

What are appropriate checklists for year-end taxplanning? Tax planners often develop checklists to guide taxpayers toward year-end strategies that might help reduce taxes. Certain tax benefits may be available if you can claim an individual as a dependent. Family taxplanning. Copyright 2022.

What are the tax challenges in secondary transactions? Secondary transactions present a specific set of tax challenges due to the nature of the investments and the structures involved. Unrelated Business Taxable Income (UBTI) UBTI is income generated by a tax-exempt organization from an unrelated trade or business.

Your contributions accumulate tax deferred, which means that you don’t pay income taxes on the earnings each year. Then, if you withdraw funds to pay the beneficiary’s qualified education expenses, the earnings portion of your withdrawal is free from federal income tax.

The FLP is used to shift present business income to lower-bracket family members. The information provided is not intended to be a substitute for specific individualized taxplanning or legal advice. We suggest that you consult with a qualified tax or legal professional. an existing business) to this entity.

This is the time to do comprehensive financial planning: retirement planning, investment planning, taxplanning and estate planning. Growth is where she begins designing her new life and starts exploring the possibilities.

The start of a new year presents opportunities for clients to make positive changes for their financial futures. According to a recent Advisor Authority survey, powered by the Nationwide Retirement Institute®, only 20% of non-retired investors have confidence in their retirement plans despite market volatility.

Significant changes are on the horizon with the upcoming sunset of the Tax Cuts and Jobs Act (TCJA) at the end of 2025. The anticipated sunset of some important provisions presents a great opportunity to start discussing steps we can take to prepare. Income Tax Changes Understand the specific changes in income tax rates and deductions.

If you’re focused on financial wellness, you’re also working on your long-term goals, and as a result, you are likely to enjoy both your present and your future more. The information provided is not intended to be a substitute for specific individualized taxplanning or legal advice.

From quarterly estimated taxplanning to equity compensation and crypto taxplanning, diversifying your service offerings can not only set you apart from the competition, it can also help you significantly grow your revenue and retain clients.

However, a period of lower income in 2024 could present valuable taxplanning opportunities. One potential benefit of a job layoff is a temporary drop in your federal income tax bracket, which can create opportunities for future tax savings.

When you are presented with the option to distribute your assets, you will have the choice to roll them into an IRA or place the stock into a taxable account and then roll the remaining assets into an IRA or 401(k). For more information on taxplanning opportunities, please get in touch with a Fortune Financial Advisor.

Are you ready to present yourself to them? Wear a suit and present yourself conservatively. “I want to upgrade my client base and work with ultra high net worth individuals and Family Office clients. How do I meet them?” ” Whoa, let’s press pause for a second. These are some of the richest families in the world.

These numbers show an opportunity for tax practices to build deeper, meaningful relationships with their clients, helping them to navigate some of life’s most challenging financial decisions. And you’ll see in our Q&A below, that tax advisors can bring estate planning into the conversation early on in a client relationship.

Of course, individuals over age 50 are usually entering their highest earning years, so no longer being able to exclude $7,500+ from income will end up costing most high earners in the form of higher taxes for the year. that presents significant hurdles for small employers. it’s clear that investors need to be adaptive in taxplanning.

Financial planning, estate planning, taxplanning, etc, rather than just picking stocks like in the old days. Facts presented have been obtained from sources believed to be reliable. But consumers do expect more for that price. So, the good news is consumers want what you have, and that’s not going away.

Instead of just talking about taxes in retirement, Joe presents a clear problem (overpaying taxes) and an actionable solution (his free video series on taxplanning through retirement). A strong hook: He immediately addresses a common pain point: Worried about taxes eroding your retirement savings?

He is a BFSI Industry Veteran with over 30 Years of Experience across various functions Financial planning is, in the words of renowned author Alan Lakein, “Bringing the future into the present so that you may do something about it now.” It also guides on building a client base and becoming a successful financial planner.

The Harness Marketplace attracts employees, founders, and investors in tech, healthcare, management consulting, and other high-earning industries who need help managing complex tax needs. Be specific to attract your ideal tax client: When it comes to what sets your firm apart, be very clear.

By shifting state tax payments to the entity level, business owners bypass the double taxation that arises when these taxes are paid individually and subjected to the SALT deduction limit.

Do you offer taxplanning as a service but manage client tax data in Microsoft Excel? eMoney Advisor is not responsible for the content, views or opinions presented by our guest, nor may eMoney Advisor be held liable for any actions taken by you based on the content, views or opinions of the guest. You catch my drift.

Aaron Parish [link] Level Wealth Stephan Shipe Home Scholar Advising Ohio Curtis Bailey quietwealth.net Flat Fee of $6,000 per year charged at $500 per month Brian Tegtmeyer Home Flat Fee financial planning, investment management, and taxplanning for new retirees. I also provide one-time retirement plans for DIY investors.

Without downplaying the importance of appropriate action around year-end taxplanning, our purpose in this letter is to encourage clients to step back, take a breath and consider using this time to focus on the long term. But, there are other considerations to keep in mind, like changes in tax exposure.

This article should not be considered tax or legal advice and is provided for informational purposes only. The information discussed and presented herein is intended to serve as a basis for further discussion with your legal, tax and/or accounting advisors. Registration does not imply a certain level of skill or training.

Then we do the financial plan and taxplanning around that—it’s been a lot of fun. Offer Tech That Enhances the Client Experience At Vincere, we’ve worked to create a tech-forward planning experience for Millennials with better integrations and interactive planning.

In addition to freezing estate tax values, this ability to exchange assets between grantor and trust is a valuable income taxplanning tool as it allows a grantor to remove low-basis assets from the trust in exchange for an equivalent value of high-basis assets contributed by the grantor.

The second headline was Edelman Financial engines closed down their tax prep services (separate/different from their taxplanning services). But they did close tax prep. And this is just a reality, which is tax implementation is time-consuming and it’s often offered because clients want more for that 1%.

Some clients opt for more aggressive gifting strategies, especially with the sunset of estate tax exemptions looming, which allows them to utilize their lifetime gift exemptions effectively. Inheritance TaxPlanning Inheritance taxes, including estate and gift taxes, are pivotal in estate planning discussions.

While these can be avoided, there is another cash outflow that can considerably lower your savings and returns and is also hard to avoid – tax. Taxplanning is essential. Tax is charged on every penny you earn. Just like the 401k, you also have other tax-advantaged accounts like the IRA. More than $1,000,000.

Unfortunately, it could also lead to larger capital gains and taxes in the future. While there may be some truth to that, it assumes consistent investment growth and accurate predictions of future capital gains tax rates. In short, the present value of current tax savings is seen as more valuable than uncertain future tax liabilities.

Taxplanning and optimization Understanding and optimizing your tax situation is an important aspect of financial planning. To reduce the amount of tax you owe and increase your savings, become familiar with income tax regulations and possible deductions.

It works like this: The present value of the calculated minimum benefit is compared to the value of the RC Account (remember this is the account into which Intel used to make matching 401(k) contributions). If the RC Account is greater than the present value of the calculated minimum benefit, there is no MPP.

Difference 4: Using taxplanning strategies While both groups are subject to the same tax laws, the wealthy often employ sophisticated legal structures and financial tools to minimize tax burdens strategically. High-net-worth individuals are adept at using legal mechanisms to optimize their taxplanning.

Overpaying on taxes. TaxPlanning. A proactive taxplan can save you thousands of dollars every year. You can accomplish this task in several ways like strategic charitable giving, maxing out your retirement accounts, tax-loss harvesting, and more. The post Why Should You Care About Financial Planning?

Material presented is believed to be from reliable sources, however, we make no representations as to its accuracy or completeness. Maxing out contributions to a 401k plan or a retirement account does not assure or guarantee better performance and cannot eliminate the risk of investment losses.

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content