This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

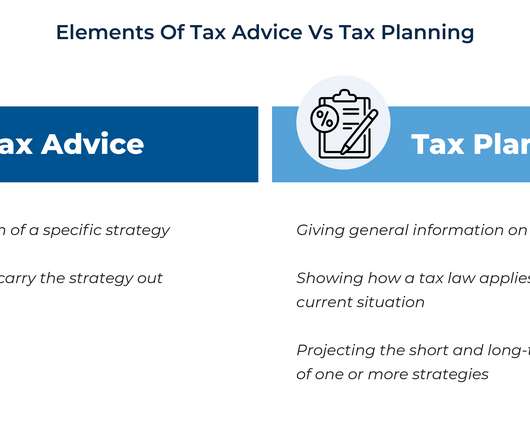

Taxes are a central component of financial planning. Almost every financial planning issue – whether it is retirement, investments, cash flow, insurance, or estate planning – has tax considerations, and advisors provide a great deal of value in helping clients minimize their overall tax burden.

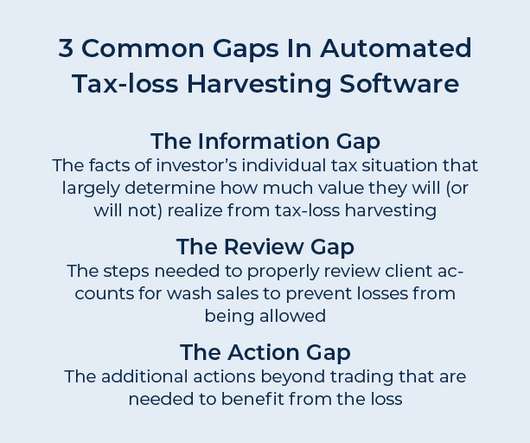

In recent years, numerous software solutions have sprung up that aim to automate the process of tax-loss harvesting. But what the providers of automated tax-loss harvesting often don’t mention is that the actual value of tax-loss harvesting depends highly on an individual’s own tax circumstances.

Tax-loss harvesting – i.e., selling investments at a loss to capture a tax deduction while re-investing the proceeds to maintain market exposure – is a popular strategy for financial advisors to increase their clients’ after-tax investment returns. With these three tools (i.e.,

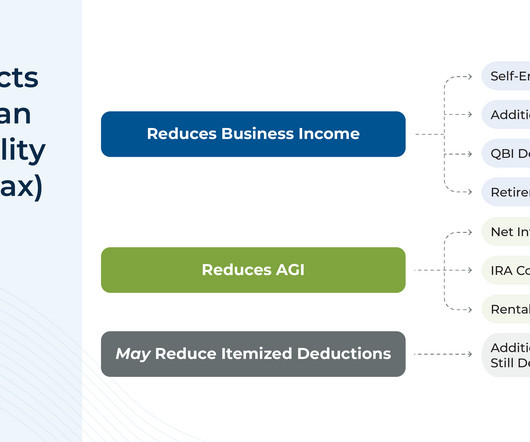

The 2017 Tax Cuts & Jobs Act introduced a $10,000 limit on the State And Local Tax (SALT) deduction that was previously available for taxpayers who itemized their deductions. Another set of considerations involves owners of businesses that operate in multiple states, which can compound the complexity of electing a PTET.

As dynamic as the secondary market may be, secondaries come with complex tax implications that can significantly impact returns if not properly managed. What are the tax implications of secondary transactions? What are the tax challenges in secondary transactions? What tax strategies optimize secondary investments?

Financial planning and taxplanning go hand in hand. Including taxplanning as part of your service provides clients a comprehensive view of their finances and helps them achieve their financial goals. Start with Document Sharing The first step is to ask your clients to share their tax documents with you.

is the projected future direction of medical care, where, instead of taking a reactive approach to disease and illness, healthcare practitioners instead invest more energy focusing on preventing illness and maintaining good health in the first place through more personalized plans for patients. Specifically, Financial Advice 3.0

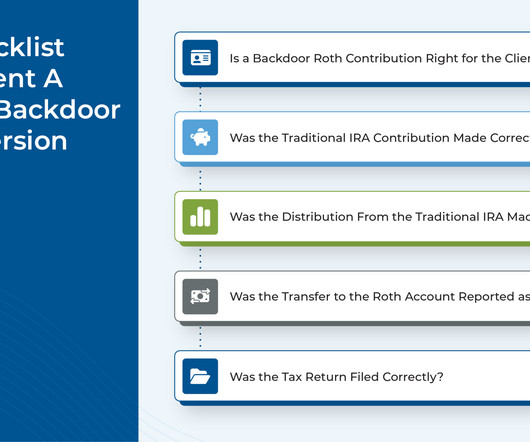

There are many taxplanning strategies that allow financial advisors to demonstrate the ongoing value they provide to clients in exchange for the fees they charge. Advisors also can support the backdoor Roth process by communicating with clients' tax preparers about the strategy and why they are recommending it for their mutual client.

Tax-loss harvesting is a powerful strategy that investors can use to reduce their taxable income. As effective as tax-loss harvesting can be, there are a number of important details that investors need to be aware of in order to implement the strategy successfully while following regulations. How does tax-loss harvesting work?

Finally, the annual T3/Inside Information Software Survey, which assesses the software programs used by financial advisors, found that taxplanning tools are on the rise – with adoption rates jumping from 30% to 43%.

When you are presented with the option to distribute your assets, you will have the choice to roll them into an IRA or place the stock into a taxable account and then roll the remaining assets into an IRA or 401(k). However, the tax deferral benefit comes at a cost tradeoff. Watch to Learn More About General Rules Surrounding NUA.

What are appropriate checklists for year-end taxplanning? Tax planners often develop checklists to guide taxpayers toward year-end strategies that might help reduce taxes. Certain tax benefits may be available if you can claim an individual as a dependent. Family taxplanning. Employee matters.

Tax season is upon us, but you can start 2024 off on the right foot with taxplanning tips and strategies presented by Mike Valenti, Director, TaxPlanning and Tom Fridrich , Carson Group Manager & Sr.

Qualified withdrawals from a 529 plan are tax-free at the federal level, and some states also offer tax breaks to their residents. It’s important to evaluate the federal and state tax consequences of plan withdrawals and contributions before you invest in a 529 plan.

Pass-Through Entity Tax (PTET) is a state-level tax mechanism designed to sidestep the federal State and Local Tax (SALT) deduction limit. Allowing a pass-through entity to pay state income taxes directly, PTET effectively shifts the tax burden from individual owners to the business itself.

Income shifting (also known as income splitting) may be defined as dividing income in a way that lowers overall taxes. When using these methods to shift income to a child, it’s always important to bear in mind the kiddie tax. Timing the receipt of your income can also help you lower your taxes.

Significant changes are on the horizon with the upcoming sunset of the Tax Cuts and Jobs Act (TCJA) at the end of 2025. The anticipated sunset of some important provisions presents a great opportunity to start discussing steps we can take to prepare. Income Tax Changes Understand the specific changes in income tax rates and deductions.

While these can be avoided, there is another cash outflow that can considerably lower your savings and returns and is also hard to avoid – tax. Taxplanning is essential. Tax is charged on every penny you earn. Tax evasion is a crime, and missing tax payments can lead to legal hassles that can be hard to get out of.

The rise of remote work and digital nomadism has made FEIE a common tax minimization strategy for Americans living abroad. What is the Foreign Tax Credit (FTC)? Financial and lifestyle considerations of living abroad The importance of professional tax advice for expats FAQs about the FEIE What is the Foreign Earned Income Exclusion?

Backdoor strategies are retirement contribution methods that allow individuals to bypass income limits and contribute to tax-advantaged retirement accounts. The strategies typically involve making after-tax contributions to a traditional IRA or 401(k), then converting those funds into a Roth IRA or Roth 401(k). Complex setup process.

From quarterly estimated taxplanning to equity compensation and crypto taxplanning, diversifying your service offerings can not only set you apart from the competition, it can also help you significantly grow your revenue and retain clients.

For instance, the Heath Walters Institute offers on-demand taxplanning and support for financial advisors who want to better serve their high-net-worth clientele.

In a recent CNBC article, our Wealth Advisor, Catalina Franco-Cicero, MS, CFP®, CTS , was quoted on the topic of tax strategies during periods of unemployment. However, a period of lower income in 2024 could present valuable taxplanning opportunities.

These numbers show an opportunity for tax practices to build deeper, meaningful relationships with their clients, helping them to navigate some of life’s most challenging financial decisions. And you’ll see in our Q&A below, that tax advisors can bring estate planning into the conversation early on in a client relationship.

In this guest post, Harness Tax Advisory Council member, Griffin Bridgers, J.D., covers some of the top estate planning trends that tax advisors should be tracking during the second half of 2024. No Step-Up in Basis for Grantor Trust Assets Grantor trusts serve as an effective tool in estate planning.

Key Takeaways: The Harness Marketplace allows your tax firm to be paired with high-value tax clients whose unique needs align with your expertise. The Harness Marketplace attracts employees, founders, and investors in tech, healthcare, management consulting, and other high-earning industries who need help managing complex tax needs.

The start of a new year presents opportunities for clients to make positive changes for their financial futures. According to a recent Advisor Authority survey, powered by the Nationwide Retirement Institute®, only 20% of non-retired investors have confidence in their retirement plans despite market volatility.

“Until I found Harness, starting my own tax practice wasn’t an option that I was seriously considering.” Due to Mr. Maddox’s relationship with Harness as a tax adviser on the platform, material conflicts of interest may arise. Maddox’s relationship with Harness as a tax adviser on the platform, material conflicts of interest may arise.

We recently connected with Michael Paley, Chief Operating Officer of Klingman & Associates , for a Q&A on how tax advisors can collaborate with wealth managers to better serve clients. Q: How can tax advisors align with the work of wealth advisors? Unlike an endowment, taxes really matter.

One major thing to consider when doing so is the tax bill that may come along with it. The good news is you may be able to take advantage of a little-known tax break called net unrealized appreciation (NUA) — if you qualify. . What Is NUA? You originally paid $10 per share but they are now valued at $50 per share. Reaching age 59 -1/2.

This is the time to do comprehensive financial planning: retirement planning, investment planning, taxplanning and estate planning. Growth is where she begins designing her new life and starts exploring the possibilities.

Navigating the complexities of estate planning can often feel like charting through uncharted waters, especially when it comes to handling assets, taxes, and ensuring one’s legacy is preserved according to their wishes. However, there are nuances to consider.

If you’re focused on financial wellness, you’re also working on your long-term goals, and as a result, you are likely to enjoy both your present and your future more. The information provided is not intended to be a substitute for specific individualized taxplanning or legal advice.

In addition to this, you can save more and plan for more significant purchases with greater ease. The tax liabilities for married couples filing their taxes jointly will differ from single individuals and those filing individually. Married couples can file their taxes jointly under the filing status of married filing jointly.

was signed into law December 29th, 2022, bringing more major changes to tax law. 529 plan to Roth IRA rollovers. The individual must be the designated beneficiary of the 529 plan and move funds to a Roth IRA in their name. Amount rolled over is tax-free (not included in beneficiary’s income) and penalty-free.

Tax and insurance advice was also somewhat constrained. ” I have this conversation all the time, explaining how an LLC has nothing to do with specific tax rules, it’s a legal structure for liability. Then we do the financial plan and taxplanning around that—it’s been a lot of fun.

Instead of just talking about taxes in retirement, Joe presents a clear problem (overpaying taxes) and an actionable solution (his free video series on taxplanning through retirement). A strong hook: He immediately addresses a common pain point: Worried about taxes eroding your retirement savings?

(Click here for Blog Archive)(Click here for Blog Index) (Presentations in this Blog were created using the Loan-Based Split-dollar System and Wealthy and Wise®) Blog #221 follows up on Blog #220, which described coupling Premium Financing with Wealthy and Wise® to produce a powerful wealth planning concept called “Zero Estate Tax.”

Retirement planning can be a bit complex. There are multiple factors to weigh in, right from healthcare and inflation to estate planning, business succession planning, taxplanning, and more. However, the main drawback to this can be the lack of foresight regarding what and how to plan.

(Click here for Blog Archive)(Click here for Blog Index) (Presentations in this Blog were created using the InsMark Loan-Based Split Dollar System) Editor’s Note: This blog presents a sizzling loan-based split-dollar plan. This executive benefit will be difficult to justify if interest rates increase considerably.

Financial planning, estate planning, taxplanning, etc, rather than just picking stocks like in the old days. Nothing in these materials is intended to serve as personalized tax and/or investment advice since the availability and effectiveness of any strategy is dependent upon your individual facts and circumstances.

The Roth IRA can be a reliable and tax-efficient way to save for your future. A Roth IRA can provide you with tax-free growth, flexible contributions, and many investment options. Retirement planning accounts like the Roth and Traditional IRAs are among two of the most commonly used instruments for retirement savings.

Do you offer taxplanning as a service but manage client tax data in Microsoft Excel? It is not meant to be, and should not be taken as financial, legal, tax or other professional advice. If your tech stack doesn’t strongly represent your service offerings, your stack needs a facelift. You catch my drift.

Furthermore, real estate investing for high-income earners can also offer tax benefits. Deductions for mortgage interest, property taxes, and depreciation can significantly mitigate their tax liabilities and enhance the appeal of real estate as an investment avenue.

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content