This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

We start with several articles on retirementplanning: Why considering a client's retirement time horizon and spending flexibility could lead to more accurate (and often higher) safe withdrawal rates than the simpler "4% rule" Four unique risks retirees face when drawing down their assets, from sequence of returns risk to tax risk, and how financial (..)

Also in industry news this week: According to a recent survey, advisors are putting an increasing share of client assets into model portfolios, allowing for customization and time savings that advisors appear to be using to provide more comprehensive planning services RIA M&A deal volume saw an annual record in 2024 as a lower cost of capital, (..)

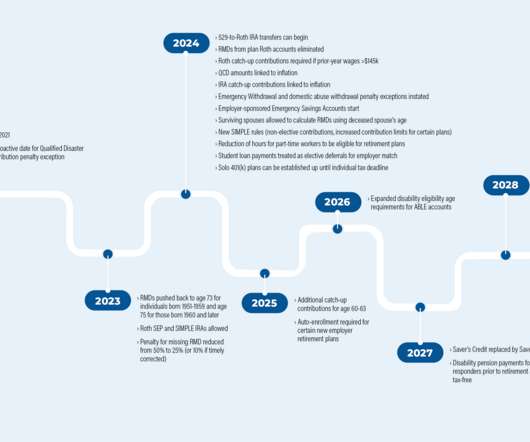

The Setting Every Community Up for Retirement Enhancement (SECURE) Act, passed in December 2019, brought a wide range of changes to the retirementplanning landscape, from the death of the ‘stretch’ IRA to raising the age for Required Minimum Distributions (RMDs) to 72. In addition, SECURE 2.0

The Setting Every Community Up for Retirement Enhancement (SECURE) Act, passed in December 2019, brought a wide range of changes to the retirementplanning landscape, from the death of the ‘stretch’ IRA to raising the age for Required Minimum Distributions (RMDs) to 72. In addition, SECURE 2.0

Like gardening or working out, taxplanning is one of those activities where you get out what you put in. Taxplanning is similar in the sense that you can put work in on the front end that youll reap benefits from later. Many of us just do tax preparation, dropping off a shoebox of documents with a CPA for the weekend.

a state’s income tax rules can have a significant impact on where they might choose to live. That’s because many states (including those typically labeled as “high-tax”) feature a slew of different tax breaks that can significantly reduce the tax burden for retirees in those states.

(citywire.com) Creative Planning is expanding its reach in the retirementplan space. papers.ssrn.com) Taxes A 2023 year-end taxplanning guide. citywire.com) Choreo is buying the wealth management business of BDO USA. investmentnews.com) M&A The RIA model continues to take share.

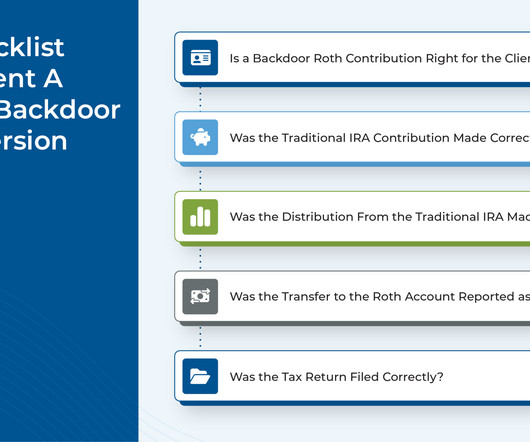

Because many taxpayers earn too much to make pre-tax IRA contributions as they have a 401(k) at work. Although any investor with earned income can make a non-deductible contribution to an IRA (up to $7,000 in 2024-2025 if under age 50) and still take advantage of tax-deferred growth, it still may not be advisable. Yes and no.

There are many taxplanning strategies that allow financial advisors to demonstrate the ongoing value they provide to clients in exchange for the fees they charge. Advisors also can support the backdoor Roth process by communicating with clients' tax preparers about the strategy and why they are recommending it for their mutual client.

Retirementplanning is a critical part of financial security that many women still overlook. However, remember that as a woman, you have a longer life expectancy than a man, which means retirementplanning is even more important. Consider early retirementtaxplanning.

Within this framework, the concept of the five pillars of retirementplanning emerges as a valuable strategy. These pillars provide a comprehensive framework for building a resilient and sustainable plan. Another important aspect of investment planning is its role in combating inflation.

In late 2019, Congress passed the Setting Every Community Up for Retirement Enhancement (SECURE) Act, introducing several significant changes to retirementplanning. This shift has led financial advisors to explore new strategies for mitigating the resulting tax-planning challenges.

Freelancers and contractors may enjoy greater flexibility and independence than full-time employees, however, this autonomy brings increased tax responsibility. Unlike W-2 employees, freelancers and independent contractors are responsible for managing their own tax obligations, which can be a complex process.

kitces.com) Taxes Following the RMD rules for inherited IRAs may not be optimal. investmentnews.com) On the importance of taxplanning in the first few years of retirement. papers.ssrn.com) Four steps to create a digital estate plan. (riabiz.com) The SEC Onsite SEC examinations are ramping up. forbes.com)

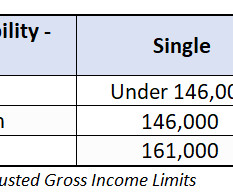

Even though retirees have contributed throughout their careers, a portion of those benefits could still be taxed, depending on your total income. Here’s how it breaks down for 2023-2024: If a couple’s total retirement income is between $32,000 and $44,000, up to 50% of Social Security benefits could be taxable.

April 15 marks the IRS tax return filing deadline for 2025. Although this is the traditional tax filing deadline, given the spate of recent natural disasters (such as the California wildfires and Hurricane Milton), the IRS is granting certain filing and payment extensions beyond this date.

Get Help with TaxPlanningTaxplanning is a critical component of financial management. Proper taxplanning can save your business money and ensure compliance with regulations. More importantly, be prepared to pay the proper taxes throughout the year.

And as 2023 draws to a close, we wanted to highlight 25 of the most popular and insightful articles that were featured throughout the year (that you might have missed!).

Why does taxplanning matter for your retirementplan? Brian talks through the difference it can make and why you should pay attention to it now as a part of your financial plan. When it comes to taxes, should you use the same person that files taxes to do taxplanning and retirementplanning for you?

This month's edition kicks off with the news that digital estate planning platform Wealth.com has raised a whopping $30 million in Series A funding, following on the heels of Vanilla's follow-on $20M capital round just a few months ago – which on the one hand reflects the anticipated enthusiasm for solutions that can help advisors efficiently (..)

When you transfer most assets to a taxable account, there will be income tax, but with company stock, you can take advantage of net unrealized appreciation (NUA). . You cannot sell the securities within the retirementplan, then move cash to a brokerage account and purchase the same shares at that point. Cost Tradeoff.

Even if a client believes they would not be subject to estate or gift tax under current law, you may want to re-examine the value of their assets to determine whether they exceed a lower exemption amount. Tax season has begun, and it’s not too early to think about planning for the 2023 tax year.

In November 2022, proponents of the Massachusetts ‘millionaires’ tax (question 1) won their bid to nearly double the income tax rate on individuals with taxable income over $1M a year. As proposed, the new legislation would increase these tax rates to 9% and perhaps even 16% , respectively, starting in 2023.

As such, one of the most important retirement income resources is Social Security, which provides retirees inflation-adjusted income for life. Making the right decisions around claiming Social Security — based on your spending needs, longevity and taxplanning — could mean the difference between meeting your retirement goals or not.

How you handle taxes and when you are taxed are two of the most important factors when it comes to retirementplanning. There are also Roth 401(k)s that have a similar tax treatment but are subject to some different rules.

The 2017 Tax Cuts and Jobs Act (TCJA) brought sweeping changes to the tax code, impacting every taxpayer and business owner. Here’s a summary of the major tax law changes coming in 2026 and some steps individuals and business owners can take to prepare. For some, this may lead to more taxes paid on capital gains.

Retirementplan savers looking to mitigate the risk of higher taxes in the future may benefit from making after-tax contributions to employer plans, which may be transferred to Roth accounts. Our Bill Cass details a “mega backdoor” Roth strategy.

What are appropriate checklists for year-end taxplanning? Tax planners often develop checklists to guide taxpayers toward year-end strategies that might help reduce taxes. Certain tax benefits may be available if you can claim an individual as a dependent. Family taxplanning. Employee matters.

Backdoor strategies are retirement contribution methods that allow individuals to bypass income limits and contribute to tax-advantaged retirement accounts. The strategies typically involve making after-tax contributions to a traditional IRA or 401(k), then converting those funds into a Roth IRA or Roth 401(k).

As you plan for retirement, it’s important to consider tax optimization strategies to minimize your tax liabilities. Here are three key ways to optimize taxes in retirement, based on information from sources published between 2022 and 2023.

Financial planning can be complicated. Have you thought about taxes or estate planning or when to withdraw and from where? From retirement income to tax strategies on an investment property, Brian shares what options you might have. (0:12) 4:06) Taxplanning plays a key role in financial planning. (7:42)

The IRS has released the 2023 contribution limits for retirementplans and other cost-of-living adjustments. The agency also released tax brackets for ordinary income and long-term capital gains. Income Limits for Tax-Deductible IRA Contributions & Roth IRA Contribution Eligibility. Income Tax Rates in 2023.

Last year’s considerable losses and market fluctuations underscore the need for clients to assess their retirementplans to ensure it aligns with their objectives, financial situations, timelines, and attitudes toward market volatility. You can help them start the year right by conducting a retirement checkup.

Your retirement income plan may be sending up bubbles, too, whether around Social Security, retirement account distributions, taxes or somewhere else – and these holes need to be patched up right away. So, to help your retirementplan be more airtight, let’s look at a few of the common leaks.

just upended retirementplanning…again. The age when retirees must begin drawing from non-Roth retirement accounts increases to 73 in 2023, then 75 in 2033. Raising the age when withdrawals must begin is great as it gives investors more planning opportunities. The Secure Act 2.0

One of those options might be to set up a defined contribution plan such as a 401(k). [1] 1] A 401(k) will allow you to set aside some of your assets into a tax-advantaged account that can have market exposure and the potential to grow over time. [2] 4] This is a tax-advantaged account, much like a 401(k). [5]

The post Part 3: Tax-Wise Financial Planning appeared first on Yardley Wealth Management, LLC. Part 3: Tax-Wise Financial Planning In our last two pieces, we covered some tools of the tax-planning trade, as well as how to deploy them for tax-efficient investing. Life happens. You buy a business.

The post Part 3: Tax-Wise Financial Planning appeared first on Yardley Wealth Management, LLC. Part 3: Tax-Wise Financial Planning. In our last two pieces, we covered some tools of the tax-planning trade, as well as how to deploy them for tax-efficient investing. . Tax-Planning Possibilities.

If you have time to dig into the details, here’s a primer on what you can do after maxing out a 401(k) including the tax advantages of each account type. If you have time to dig into the details, here’s a primer on what you can do after maxing out a 401(k) including the tax advantages of each account type.

It doesn’t factor in your healthcare coverage situation, it isn’t designed to avoid the 3 strikes of taxplanning , and it doesn’t account for the location and liquidity of your wealth and savings. There are many moving parts to a retirementplan that must be considered if your goal is to make the most of your savings.

This is the time to do comprehensive financial planning: retirementplanning, investment planning, taxplanning and estate planning. Help her focus on immediate needs, pay bills, monitor cash flow and review her investment portfolio.

The post Part 1: The Tools of the Tax-Planning Trade appeared first on Yardley Wealth Management, LLC. Part 1: The Tools of the Tax-Planning Trade Whether you’re saving, investing, spending, bequeathing, or receiving wealth, there’s scarcely a move you can make without considering how taxes might influence the outcome.

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content