This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Saving for retirement is a major undertaking for most of us. Health savings accounts (HSA) provide another vehicle to save for retirement. Many of you have the option to enroll in high-deductible insurance plans that allow the use of a health savings account via your employer. The rising cost of healthcare in retirement .

By Jake Anderson, CFP ® , Wealth Planner When helping clients begin retirementplanning, the same questions often arise: What should my retirementplan look like? Your lifestyle, goals, family situation, and risktolerance will give a unique signature to your retirementplan.

But despite recognizing the impact of investment variability and sequence of return risk on a financial plan, advisors have generally ignored the same historical trends for inflation in their clients' financial plans.

Podcasts Christine Benz and Jeff Ptak discuss the recent "The State of Retirement Income" report. peterlazaroff.com) Risktolerance Five behavioral tricks for long-term investors including 'Have a small side account.' bestinterest.blog) On the difference between risktolerance and risk perception.

This month's edition kicks off with the news that Riskalyze has completed its previously-announced rebranding, and will now be known as “Nitrogen”, a ”growth platform” for advisory firms – which represents less of a shift in the platform’s core function (given that Riskalyze’s risktolerance tool was always (..)

But despite recognizing the impact of investment variability and sequence of return risk on a financial plan, advisors have generally ignored the same historical trends for inflation in their clients' financial plans.

Historically, advisors haven't had many avenues to manage clients' 401(k) plan accounts, since unlike traditional custodial investment accounts, advisors generally lack discretionary trading authority in employer-sponsored retirementplans.

Achieving financial freedom in retirement requires meticulous planning, dedicated effort, and strategic management. Without a solid plan, you risk drifting without direction. Within this framework, the concept of the five pillars of retirementplanning emerges as a valuable strategy.

Historically, advisors haven't had many avenues to manage clients' 401(k) plan accounts, since unlike traditional custodial investment accounts, advisors generally lack discretionary trading authority in employer-sponsored retirementplans.

How much do I need for retirement?” Your financial needs in retirement can depend on dozens of factors – some known and some unknown. One or two million dollars may seem like a lot of money to have set aside for retirement. A Retirement Reality Check. The concept of retirement continues to evolve with the world around us.

The idea of living off dividends in retirement sounds nice, but investors often don’t realize how much money they’ll need invested to generate enough income from dividends to cover lifestyle expenses. You may need more money than you think to retire on dividends. Retire on dividends?

As someone saving for retirement , what should you do now? The PBS Frontline special The Retirement Gamble put much of the blame on Wall Street and they are right to an extent, especially as it pertains to the overall market drop. If so, this is a good time to revisit your asset allocation and perhaps reduce your overall risk.

decreasing withdrawals if market returns are weak and the probability of success falls, or vice versa), making them somewhat less useful for ongoing planning engagements where an advisor could recommend spending changes if they become necessary.

Assuming that you have a financial plan with an investment strategy in place there is really nothing to do at this point. Ideally you’ve been rebalancing your portfolio along the way and your asset allocation is largely in line with your plan and your risktolerance. Focus on risk. Be a smart investor.

Early retirement has become a popular financial goal. Even if you never retire early, just knowing that you can is liberating! Can You Really Retire at 50? Can You Really Retire at 50? Table of Contents Can You Really Retire at 50? FAQs on Retiring Early at 50 It’s a big bold claim – retire at 50?

Last year’s considerable losses and market fluctuations underscore the need for clients to assess their retirementplans to ensure it aligns with their objectives, financial situations, timelines, and attitudes toward market volatility. You can help them start the year right by conducting a retirement checkup.

Saving for retirement is a long-term endeavor. It requires a different perspective on your wealth and income that accounts for your needs in different stages of your life, from the beginning of your working years through your retirement. The Risk Bucket. The Safe Bucket. The Spend Bucket. The Importance of Balance.

Navigating the journey to retirement can often feel like a complex puzzle, especially when it comes to figuring out how much you need to save. The answer to “how much you need to retire” is shaped by various factors, including the kind of retirement life you dream of, your age, and the expenses you anticipate during your retirement years.

The choice between stocks and bonds depends on their individual circumstances, such as risktolerance, time horizon, and financial goals. While an investor’s timeline affects their risktolerance and allocation decisions between stocks and bonds, it’s important to remember how long a retirement time horizon can truly be.

Rather I suggest an investment strategy that incorporates some basic blocking and tackling: A financial plan should be the basis of your strategy. Any investment strategy that does not incorporate your goals, time horizon, and risktolerance is flawed. Approaching retirement and want another opinion on where you stand?

1 With ever-increasing life expectancies, it’s no wonder 63% of American adults say they’re more afraid of running out of money in retirement than they are of death. 2 That’s why it’s vitally important to consider longevity risk when you’re planning for your financial needs in retirement. What Is Longevity Risk?

Retirement is an exciting milestone—a time to leave behind the hustle and bustle of work and embrace a new chapter filled with more freedom and opportunities to enjoy life. Planning well in advance ensures that your retirement years will be financially secure, fulfilling, and less stressful than your working years.

Starting early with investing for retirement is so important to secure your future self. This means that saving for retirement should be a component of your overall financial portfolio and wealth-building strategy. So, let’s discuss how to save for retirement in your 20s! The 401(k) Plan 2. Traditional IRA 3.

While grappling with various aspects of retirementplanning, it is imperative to acknowledge a critical factor that often does not receive its due attention – longevity risk. Longevity risk refers to the risk that people are living longer lifespans than previous generations.

The same way you prepare for the winter, you might have to prepare your retirement finances for a potential recessionary period. There is no simple fix for getting ready for a rocky economy – what is right for you may vary based on your unique financial situation, goals, and retirement timelines. What Can We Expect from the Markets?

The reality for those with various employers is that untracked retirement savings might lead to missed financial growth opportunities and instability. Diligent oversight and management of these retirement accounts is essential for anyone aiming to build a solid financial foundation for a comfortable and secure retirement.

A Contributory IRA, otherwise known as a traditional IRA , is a retirement savings account that allows individuals to make contributions from their earned income. The contribution limit may be reduced or eliminated for individuals who have high incomes or who participate in an employer-sponsored retirementplan.

This advanced language processing technology has also greatly impacted the financial advisory sector, prompting a critical question: Can ChatGPT replace human financial advisors in retirementplanning? Personalized guidance, empathy, and a deep contextual understanding are integral to effective retirementplanning.

While they do share some similarities, there are enough distinct differences between the two where they can just as easily qualify as completely separate and distinct retirementplans. Either plan is an excellent choice, particularly if you’re not covered by an employer-sponsored retirementplan. Not exactly.

Take Advantage of RetirementPlans and Matching Contributions. Most employer retirementplans allow you to save on a tax-deferred basis, meaning that contributions into these types of accounts are not considered in calculating your taxable income. . Determine an Appropriate RiskTolerance for a Longer Time Horizon .

According to a survey, a significant majority of Americans, approximately 80%, share the common notion that the point of working hard in your adult life is so you can enjoy a nice retirement. After years of dedicated labor and hard work, the prospect of a peaceful retirement appeals to everyone.

Investing in an Individual Retirement Account (IRA) is an excellent way to save for retirement. Traditional IRAs offer immediate tax breaks, while Roth IRAs offer tax-free withdrawals in retirement. Your goals may be different depending on your age, retirement timeline, and lifestyle.

Investment strategy: Determine asset allocation and investment vehicles aligned with risktolerance and financial goals. Retirementplanning: Calculate retirement needs and contribute regularly to retirement accounts. 2 In either scenario, having a plan in place can lessen the financial burden.

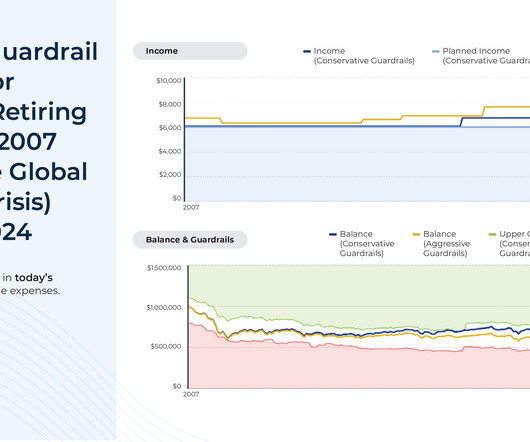

For people nearing retirement, these challenges can be even more daunting. A market downturn at the start of retirement, hitting portfolio values when retirees begin to take account withdrawals, can be unsettling, even for seasoned investors. Many near-retirees see their highest portfolio values just before retirement.

With our deep expertise and qualifications in NUA strategies, our experts are adept at navigating the complexities of tax-efficient retirementplanning. Explore the Fortune Financial advantage in transforming how you manage your retirement assets and bringing you closer to achieving your financial dreams.

And how does it compare to the 401k and other retirementplans that exist? A Simple IRA, or Savings Incentive Match Plan for Employees, is a type of employer-sponsored retirement savings plan that is designed to be easy to set up and maintain for small business owners. What is a Simple IRA?

We all know retirement is an important milestone that requires careful planning. Of course, one of the most important aspects of retirementplanning is managing retirement taxes. Taxes can significantly impact the amount of money you’ll have for retirement. This can be a mistake.

We all know retirement is an important milestone that requires careful planning. Of course, one of the most important aspects of retirementplanning is managing retirement taxes. Taxes can significantly impact the amount of money you’ll have for retirement. This can be a mistake.

Preparing for retirement is a significant life transition that demands a clear understanding of your financial situation. This data can serve as a baseline for tailoring your retirementplan, taking into account factors such as inflation, your current age, and your desired retirement age.

In our planning with clients, we like to employ a “pay yourself first” approach, especially as it relates to retirementplanning. This cycle can repeat itself over multiple years, resulting in minimal or no retirement savings. Planning for retirement is a multi-step process with continuous updates and monitoring.

Traditional IRA: Best for Dedicated RetirementPlanning. IRA plans are subject to Required Minimum Distributions (RMDs) beginning at age 72. Roth IRA: Best for RetirementPlanning + Immediate Funds Access. In addition, Roth IRAs are the only retirementplan that’s not subject to RMDs. Ads by Money.

Blind spots in retirementplanning are those aspects that are often overlooked, either intentionally or subconsciously. From seemingly harmless low-interest debt to underestimating the emotional impact of transitioning out of the workforce, various factors can disrupt your peace of mind during your retirement years.

When we are busy working to earn a living and spending time with our family, first thing needs to think about is RetirementPlanning. Generally, people think about Retirementplanning after retirement. To plan for retired life important thing is financial plan. How much will be enough?

These are all interesting and important questions, but preparation for retirement is much more important than panicking over issues you have no control over. For many investors, however, the more important questions to ask and answer relate to your retirement strategy. RiskTolerance: What is your asset allocation?

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content