This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

artofmanliness.com) Ben Carlson talks about the state of the retirement savings market with Shawn O'Brien, Director of Retirement at Cerulli Associates. riabiz.com) Risktolerance Determining a client's risktolerance is more complicated than having them fill out a questionnaire.

It's natural for advisors to begin discovery meetings by asking questions about a client's current financial situation – understanding cash flow, debt, investments, risktolerance, or even the burning tax concern that brought them to the advisor's door in the first place is crucial for financial planning.

(crr.bc.edu) What do (different) surveys tell us about well-being in retirement? wealthmanagement.com) Parsing the differences in risktolerance for a couple is tricky. crr.bc.edu) The widow tax is real. thinkadvisor.com) Advisers The RIA model continues to take share. citywire.com) Flourish is buying Sora.

Category: Clients Risk. Determining the client’s risktolerance is not an exact science and requires you to communicate with your client. What Does The Word “Risk” Mean For Your Clients? For some clients, “risk” maybe something exciting or daring that they enjoy and not something they generally avert from.

But despite recognizing the impact of investment variability and sequence of return risk on a financial plan, advisors have generally ignored the same historical trends for inflation in their clients' financial plans.

Also in industry news this week: 43% of wealth management firms are frustrated with the effectiveness of their CRM software, spurred on by challenges with integrations and workflows, according to a recent survey The Social Security Administration this week announced a 2.5%

Saving for retirement is a major undertaking for most of us. Health savings accounts (HSA) provide another vehicle to save for retirement. An HSA can serve as an additional retirement savings vehicle on top of your IRA or 401(k) to help cover healthcare and other retirement expenses. Qualified medical expenses .

This month's edition kicks off with the news that Riskalyze has completed its previously-announced rebranding, and will now be known as “Nitrogen”, a ”growth platform” for advisory firms – which represents less of a shift in the platform’s core function (given that Riskalyze’s risktolerance tool was always (..)

The idea of living off dividends in retirement sounds nice, but investors often don’t realize how much money they’ll need invested to generate enough income from dividends to cover lifestyle expenses. You may need more money than you think to retire on dividends. Retire on dividends?

kitces.com) Christine Benz and Jeff Ptak discuss the recent "The State of Retirement Income" report. nytimes.com) Retirement How to optimize Social Security benefits as a widow. mikemelissinos.substack.com) On the difference between risktolerance and risk perception. morningstar.com) SECURE Act 2.0

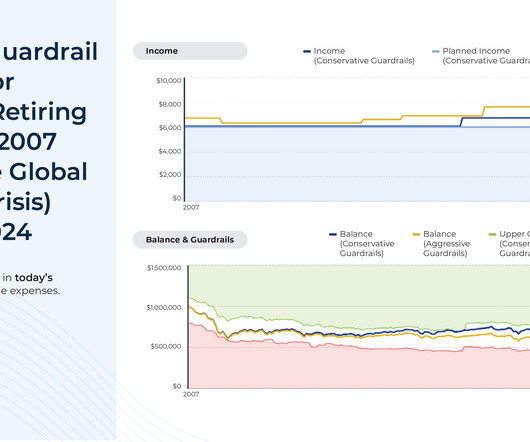

With this in mind, retirement income guardrails, which provide strategies that pre-determine when spending retirement adjustments would be made and the spending adjustments themselves – have become increasingly popular.

But despite recognizing the impact of investment variability and sequence of return risk on a financial plan, advisors have generally ignored the same historical trends for inflation in their clients' financial plans.

As someone saving for retirement , what should you do now? The PBS Frontline special The Retirement Gamble put much of the blame on Wall Street and they are right to an extent, especially as it pertains to the overall market drop. If so, this is a good time to revisit your asset allocation and perhaps reduce your overall risk.

Historically, advisors haven't had many avenues to manage clients' 401(k) plan accounts, since unlike traditional custodial investment accounts, advisors generally lack discretionary trading authority in employer-sponsored retirement plans.

Historically, advisors haven't had many avenues to manage clients' 401(k) plan accounts, since unlike traditional custodial investment accounts, advisors generally lack discretionary trading authority in employer-sponsored retirement plans.

It is essential to choose investments that match your risk appetite to avoid unnecessary stress and surprises later. A financial advisor can help you understand your investment risktolerance. This article will focus on the risks of investing, how they impact you, and what you can do to determine your risk appetite.

Ideally you’ve been rebalancing your portfolio along the way and your asset allocation is largely in line with your plan and your risktolerance. Focus on risk. Use stock market corrections and downturns to assess your portfolio’s risk and more importantly your risktolerance. Be a smart investor.

Early retirement has become a popular financial goal. Even if you never retire early, just knowing that you can is liberating! Can You Really Retire at 50? Can You Really Retire at 50? Table of Contents Can You Really Retire at 50? FAQs on Retiring Early at 50 It’s a big bold claim – retire at 50?

When talking about retirement financial planning, we often take investment strategy at face value. When it comes to retirement, there’s another aspect of income generation that is introduced. When it comes to retirement, there’s another aspect of income generation that is introduced.

For more years than I’d care to name, I’ve been trying to put my finger on exactly why I have a such a huge problem with the traditional (Think: Riskalyze, now Nitrogen) risktolerance assessments in the financial planning profession. You can actually test various bear markets and adjust accordingly.)

Saving for retirement is a long-term endeavor. It requires a different perspective on your wealth and income that accounts for your needs in different stages of your life, from the beginning of your working years through your retirement. The Risk Bucket. The Safe Bucket. The Spend Bucket. The Importance of Balance.

Financial advisors play a crucial role in assisting you before your retire. They can assess your financial situation, long-term goals, risktolerance, and investment preferences to create personalized strategies. Here are 5 benefits of hiring a financial advisor after you retire: 1.

Starting early with investing for retirement is so important to secure your future self. This means that saving for retirement should be a component of your overall financial portfolio and wealth-building strategy. So, let’s discuss how to save for retirement in your 20s! How do I start putting money away for retirement?

How much do I need for retirement?” Your financial needs in retirement can depend on dozens of factors – some known and some unknown. One or two million dollars may seem like a lot of money to have set aside for retirement. A Retirement Reality Check. The concept of retirement continues to evolve with the world around us.

Retirement is an exciting milestone—a time to leave behind the hustle and bustle of work and embrace a new chapter filled with more freedom and opportunities to enjoy life. Planning well in advance ensures that your retirement years will be financially secure, fulfilling, and less stressful than your working years.

The choice between stocks and bonds depends on their individual circumstances, such as risktolerance, time horizon, and financial goals. While an investor’s timeline affects their risktolerance and allocation decisions between stocks and bonds, it’s important to remember how long a retirement time horizon can truly be.

Navigating the journey to retirement can often feel like a complex puzzle, especially when it comes to figuring out how much you need to save. The answer to “how much you need to retire” is shaped by various factors, including the kind of retirement life you dream of, your age, and the expenses you anticipate during your retirement years.

Any investment strategy that does not incorporate your goals, time horizon, and risktolerance is flawed. Your investment strategy should be guided by your goals, your time horizon for the money and your tolerance for risk, not the outcome of a football game. Take stock of where you are. NEW SERVICE – Financial Coaching.

Last year’s considerable losses and market fluctuations underscore the need for clients to assess their retirement plans to ensure it aligns with their objectives, financial situations, timelines, and attitudes toward market volatility. You can help them start the year right by conducting a retirement checkup.

As stock prices swing and the cost of everyday goods edges upward, the uncertainty can feel overwhelming, especially for those who rely on a fixed income in retirement. The overall theme that were really getting at is you really have to be aware of your risktolerance and your financial plan, Chad shared.

Although annuities can offer a guaranteed income stream in retirement, they come with significant risks and complexities. It's essential to thoroughly understand these products and consider whether they align with your financial goals and risktolerance.

By assigning clear purposes and timelines to each bucket, you help minimize behavioral risks like selling assets during market dips with the goal of helping your investments align with your priorities. By evaluating your risktolerance, goals, and timeline, they can recommend the right mix of assets for each bucket.

Common accounts that earn this sort of income include retirement accounts, like a 401(k) or IRA , savings accounts , or a general brokerage account that lets you sell and buy investment products like stocks, funds, etc. At the same time, you lower your exposure to the risks of each. Risktolerance is simply a preference.

Investing in an Individual Retirement Account (IRA) is an excellent way to save for retirement. Traditional IRAs offer immediate tax breaks, while Roth IRAs offer tax-free withdrawals in retirement. Your goals may be different depending on your age, retirement timeline, and lifestyle.

Each has unique benefits and drawbacks, and understanding these can help you decide which fits best with your financial situation, risktolerance, and goals. Roth IRAs Roth IRAs are individual retirement accounts that offer unique advantages for both retirement and education savings.

However, it should be well understood that a client’s financial profile includes their risktolerance and their risk capacity. In this article, although we will be focusing on the latter one and why it is significant to determine your client’s risk capacity let’s first understand the difference between the two.

Category: Clients Risk. When it comes to their investment portfolios many tend to have a low-risktolerance and with the unsettling economic situation with the ongoing pandemic, the word “risk” has become even more of a fearsome word for clients. Would they consider a 5% return worth taking a risk or 20%?

[CDATA[ When you last did your projections for retirement through the tools offered from your 401(k) plan or the book your financial advisor put together, are you sure the assumptions that were made were explained to you clearly?

Which means that longer-term projects, such as creating a succession plan to have in place for the firm when the owner retires, may tend to get put on the back burner.

For people nearing retirement, these challenges can be even more daunting. A market downturn at the start of retirement, hitting portfolio values when retirees begin to take account withdrawals, can be unsettling, even for seasoned investors. Many near-retirees see their highest portfolio values just before retirement.

According to a survey, a significant majority of Americans, approximately 80%, share the common notion that the point of working hard in your adult life is so you can enjoy a nice retirement. After years of dedicated labor and hard work, the prospect of a peaceful retirement appeals to everyone.

The same way you prepare for the winter, you might have to prepare your retirement finances for a potential recessionary period. There is no simple fix for getting ready for a rocky economy – what is right for you may vary based on your unique financial situation, goals, and retirement timelines. What Can We Expect from the Markets?

The reality for those with various employers is that untracked retirement savings might lead to missed financial growth opportunities and instability. Diligent oversight and management of these retirement accounts is essential for anyone aiming to build a solid financial foundation for a comfortable and secure retirement.

Does it match your risktolerance level? For those of us who don’t feel the same level of flexibility to jump in and out of retirement, what are your options? Brian says you might not be ready to retire, but maybe you can find a different job that’s a better fit until your finances are in line.

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content