This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

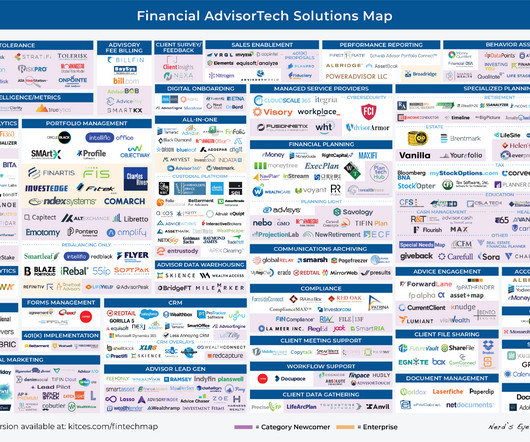

This month's edition kicks off with the news that Riskalyze has completed its previously-announced rebranding, and will now be known as “Nitrogen”, a ”growth platform” for advisory firms – which represents less of a shift in the platform’s core function (given that Riskalyze’s risktolerance tool was always (..)

Ideally you’ve been rebalancing your portfolio along the way and your asset allocation is largely in line with your plan and your risktolerance. Focus on risk. Use stock market corrections and downturns to assess your portfolio’s risk and more importantly your risktolerance. Be a smart investor.

Common accounts that earn this sort of income include retirement accounts, like a 401(k) or IRA , savings accounts , or a general brokerage account that lets you sell and buy investment products like stocks, funds, etc. Passive income is money you get from a hands-off venture, such as publishing an eBook and earning money with each sale.

However, it should be well understood that a client’s financial profile includes their risktolerance and their risk capacity. In this article, although we will be focusing on the latter one and why it is significant to determine your client’s risk capacity let’s first understand the difference between the two.

Which means that longer-term projects, such as creating a succession plan to have in place for the firm when the owner retires, may tend to get put on the back burner. Key components of this transition include client service oversight, sales oversight, strategy leadership, and financial management.

Importantly, we do not accept sales commissions or any compensation beyond what is directly agreed upon with our clients. No Product Sales, Pure Expertise: This is probably the most distinctive part of being a Garrett Planning Network advisor. Pay for Value, Not Time: Clients pay only for the time your advisor actively works with you.

The reality for those with various employers is that untracked retirement savings might lead to missed financial growth opportunities and instability. Diligent oversight and management of these retirement accounts is essential for anyone aiming to build a solid financial foundation for a comfortable and secure retirement.

Minimum Investment: Typically, 20% of the purchase price; as low as $10 with real estate crowdfunding Stability/Risk Level: High stability/moderate risk Liquidity Level: Low Transaction Costs: Up to 10% of property sale; 2% – 3% real estate crowdfunding fees Where to Invest: Your local real estate market or Fundrise (real estate crowdfunding).

Invest in the Stock Market Suggested Allocation: 40% to 50% Risk Level: Varies Investing Goal: Long-term growth The stock market is where most of us save for retirement already, mostly through the use of tax-advantaged retirement plans, like a 401(k), SEP IRA, or Solo 401(k).

Most people feel a sense of anticipation and excitement before retirement. Yet, amidst the joy and delight, it is vital to remember that the journey to retirement is not one to be rushed. Hasty decisions made before retirement can lead to unexpected financial troubles and compromises.

When failure is not an option However, where we are in our life cycle largely determines just how much risk we can take and whether we have the time necessary to pick up the pieces in the event of failure. If you’re reading this and approaching or in retirement, you’re going to need a different solution.

The downside to highly liquid investments 12 Highly liquid vs short term highly liquid investments Expert tip: Know your risktolerance When does it make sense to pursue a liquid investment? This is why preparing for retirement is about more than just saving cash—it’s about investing wisely with various types of investments.

Re-examine RiskTolerance Volatile markets may cause your clients to rethink their risktolerance, especially those who are close to retirement. When the market is down, Roth conversions are essentially on sale.

Like other similar products, they first determine your risktolerance, personal preferences, and investment goals. Retirement Planner You can often find retirement planners or retirement calculators on various sites throughout the Internet. And that’s a huge win we can all settle for.

Investment advisors analyze market trends, assess the client’s economic situation, and develop personalized investment strategies tailored to their goals and risktolerance. Investment advisors can also specialize in specific areas such as retirement planning, tax planning, or portfolio management.

Whether the windfall was expected, perhaps from the sale of a business, or unexpected, you’ll want to make a plan for the future. And ultimately, how to invest a windfall will depend on a number of factors, including your risktolerance, time horizon, and spending plans. Do you want to retire? Can you afford to?

Whether the windfall was expected, perhaps from the sale of a business, or unexpected, you’ll want to make a plan for the future. And ultimately, how to invest a windfall will depend on a number of factors, including your risktolerance, time horizon, and spending plans. Do you want to retire? Can you afford to?

The goal is to enhance the company’s financial performance, increase its value and ultimately generate attractive returns upon exit, such as through a sale or initial public offering (IPO). Each of these alternative investment options offers its own set of risks and rewards. between 2015 and the end of 2021.

The goal is to enhance the company’s financial performance, increase its value and ultimately generate attractive returns upon exit, such as through a sale or initial public offering (IPO). Each of these alternative investment options offers its own set of risks and rewards. between 2015 and the end of 2021.

An author spends many months toiling away at their latest novel, but once it’s published, they can sit back and enjoy the steady stream of royalty income from their share of book sales. With a print book, a publisher might pay you royalties for the distribution and sale of the book. The same goes for songwriters.

to +1.3% , and pending home sales dropped by -7.7% It requires patience, discipline, and financial emotional wherewithal to allow the power of long-term compounding to grow your retirement nest egg. Short-term news cycle headlines shouldn’t drive portfolio decision-making, but rather your personal objectives, goals, and risktolerance.

Imagine you make enough money through investments and savings that you can retire early. Keep working toward financial independence Related posts on financial independence We'll discuss how you can become financially independent to retire early through the FIRE (financial independence, retire early) method. What is FIRE?

Open a Roth IRA Risk level : Varies A Roth IRA is a type of retirement account you can open in addition to other accounts you have like a workplace 401(k). This type of retirement account lets you invest with after-tax dollars, and your money grows tax-free until you are ready to access it.

Not saving any of your monthly income When it comes to saving money, I’ve heard so many people complain that after they’ve paid their bills, they don’t have any money to contribute to their retirement accounts or to add to their emergency fund. But if you don’t invest, your money will not grow.

Alternatively, you may want to exercise and sell ISOs if you have a financial goal you want to fund, such as retirement, a second home, or a college expense. First and foremost, you will see the proceeds from the sale hit your account as cash. In other words, it’s any sale that doesn’t meet both holding period requirements.

Real estate investing takes work and can be risky, and many don’t have the time or risktolerance to commit. It’s also worth noting that you can use the marketplace to sell your home and only pay a final 3% sale fee. Lets’ take a closer look at some other noteworthy services Roofstock offers its users: Retirement Accounts.

A strong savings rate relative to your income can help you build reserves before retirement—and during retirement, the focus should be maintaining a reasonable and flexible withdrawal rate relative to your investable assets. Taxpayers must refrain from buying the fund (or something similar) for 30 days to avoid a wash sale.

Qualifying Dispositions/Tax Rates: To make a qualifying disposition, the final stock sale must occur: At least 2 years past the ISO grant date, AND. If you meet these hurdles, any gain on the stock sale is taxed at favorable long-term capital gains rates. First, let’s review how ISO dispositions work in general.

Knowing the types of financial advisors and their compensation models can empower you to select a professional whose approach aligns seamlessly with your financial goals, risktolerance, and overall budget. Below are the different types of financial advisors you can choose from based on their fee model: 1.

Needs: If you need the stock’s current value to fund your current lifestyle or eventual retirement, think carefully about whether you can afford to continue putting that present value at risk. First, you’ll want to be aware of any sale restrictions that apply to you , such as lock-up or blackout periods when you cannot sell.

It is essential for your investment portfolio to align with your unique financial goals, risktolerance, and time horizon. Similarly, the professional may advise investing in different instruments for goals such as retirement planning, funding your children’s education expenses, buying a home, or other objectives.

In the United States, all profits made from the purchases and sales of crypto assets such as Bitcoin, Ethereum and NFTs are subject to capital gains taxes (including airdrops). In any case, it’s worthwhile to evaluate your retirement savings strategy and optimize according to your risktolerance and lower tax burden.

Furthermore, long-term investment strategies can also provide a source of passive income, which can help to support your lifestyle before and after retirement. This improves the investment’s overall liquidity and offers more flexibility in use, purchase, and sale. Blockchain is the underlying technology for most cryptocurrencies.

KRISTEN BITTERLY MICHELL, HEAD OF NORTH AMERICAN INVESTMENTS, CITI GLOBAL WEALTH: It’s really interesting because I’m not someone that you would think would be the typical profile to end up in capital markets or — or sales and trading. BITTERLY MICHELL: … this isn’t a generalization, but they have a higher risktolerance.

Most advisors that work with commission-based income will need an individual retirement account (IRA). Whether you’re starting a new business, buying a home, or saving for retirement, you need expert advice to succeed. This is a complicated process that involves a number of questions. Organization. Accountability. Objectivity.

Windfall money might materialize in the form of gifts, bonuses, settlements, inheritances, lottery winnings, property sales, etc. That might include assessing your risktolerance, helping you build an investment strategy, or figuring out how to save money for short-term objectives.

As wealthy investors seek to safeguard their retirement savings from market volatility and currency devaluation, precious metals offer a reliable hedge against inflation and currency depreciation. Opening a gold or silver Individual Retirement Account (IRA) is another way wealthy individuals invest in gold.

Since those in non-income tax states often pay higher property or sales taxes, a state 529 plan may not be the best fit. The good news is that many 529 plans use a low risktolerance to determine their fund allocations. Additionally, you should consider your future plans before committing to a 529 plan.

I don’t know when to retire or claim Social Security. For him, DIY investors on path to retiring in 5 years How do I want to serve? Instead, he provides them with an analysis of their risktolerance and investment plan, and even specific tickers. Do I have enough to retire? What the heck is going on? In what order?

Even in retirement accounts held with Vanguard, TIPS can be purchased. In that sense, assuming you already have an existing brokerage or retirement account set up, TIPS are easier to buy than I Bonds. And if you buy them, buy them as an ETF in your brokerage or retirement account, as many individual investors do.

Can you build a centralized global sales team? But I, I, if you are on a variable comp system, depending on how successful you raise assets, it’s there in black and white on the sales log, you’ve raised X, Hey, do I really need to tell you? She’s now retired. 00:14:41 [Speaker Changed] Interesting.

Options trading is becoming increasingly popular, especially as investors look for new and different strategies to improve retirement portfolio performance. Options trading is a higher-risk activity than other types of investing, but it can be profitable if you are knowledgeable and understand those risks. Get Started.

To define your target audience, consider things like age, income, investment goals, risktolerance, job, and lifestyle. It helps them talk to clients, share useful info, and increase sales. These could include subjects like retirement planning, investment strategies, or estate planning. This can help you get better leads.

Both ISOs and NSOs follow vesting schedules that determine when options become exercisable, with taxation occurring at exercise and sale points. Early sales trigger “disqualifying dispositions” that result in ordinary income treatment reported on W-2 forms. The path to optimal tax treatment requires careful timing.

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content