This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

As the year comes to a close, now is the time to review potential financial moves to help minimize your tax burden heading into 2025. Proactive year-end taxplanning can lead to significant savings and set you up for financial success in the new year.

riaintel.com) How to prep an RIA for sale. (fa-mag.com) papers.ssrn.com) Taxes A 2023 year-end taxplanning guide. kitces.com) Advisers How the profession of financial planning has changed over time. (citywire.com) Choreo is buying the wealth management business of BDO USA. fa-mag.com) Research into how RIAs grow.

Also in industry news this week: A recent survey indicates that a strong majority of financial advisory clients have maintained their trust in their advisors despite the investment market setbacks experienced last year A report from the SEC shows that a majority RIAs have mandatory arbitration clauses in their client agreements, a practice that has (..)

And to complicate things further, when it is decided to go ahead with tax-loss harvesting, there are numerous considerations involved to ensure the strategy is carried out correctly and avoids running afoul of the IRS’s wash sale rules (which could disallow losses and negate the value of the strategy altogether).

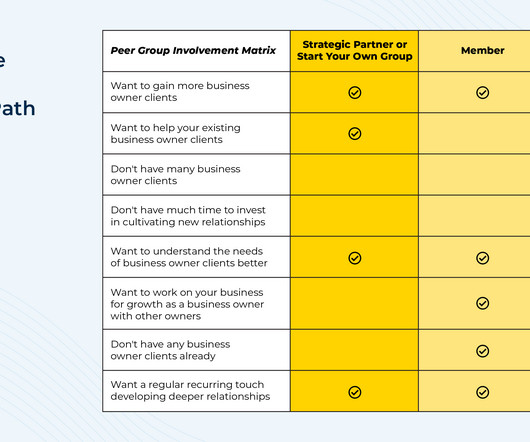

When it comes to focusing on a niche for financial advisors, business owner clients can be an appealing target as they can have complex financial planning problems ranging from cash flow management to taxplanning to acquisition strategies.

House of Representatives and is now being considered in the Senate would increase the number of firms classified as “small entities” and would require the SEC to assess the impact of proposed regulation on this newly enlarged class of investment advisers (which tend to have fewer compliance staff and resources available compared to larger (..)

As December unfolds, it’s easy to overlook year-end taxplanning amid the holiday hustle. However, dedicating a few moments now can lead to significant savings come tax season. To help you retain more of your hard-earned money and reduce your tax liability, consider these five strategic moves before the year concludes.

While clients are thinking about 2022’s taxes, it’s a good time to discuss income, estate, and business planning opportunities for 2023. Defer income Clients may consider putting off asset sales or delaying receipt of other income until next year to reduce 2023 taxable income.

There are many reasons for LP sales, but some include an LP seeking liquidity or an exit from a fund thats underperforming. GP-led secondaries can also encompass “stapled transactions” where the sale of the existing fund interest is linked to an allocation in a new fund managed by the same GP. property interests.

This month's edition kicks off with the news that custodial platform Altruist is eliminating the $1 per account monthly fee for its portfolio management and reporting technology for advisors on its platform, which on the one hand suggests that the economies of scale Altruist has achieved in the wake of its move to become a fully self-clearing custodian (..)

This month's edition kicks off with the news that digital estate planning platform Wealth.com has raised a whopping $30 million in Series A funding, following on the heels of Vanilla's follow-on $20M capital round just a few months ago – which on the one hand reflects the anticipated enthusiasm for solutions that can help advisors efficiently (..)

Cost-saving taxplanning can be much more difficult to implement after your company is well-established and has reached the stage where an IPO, merger, or acquisition becomes a likely event. Sale price per share $15.00 $15.00 Sale price per share $15.00 $15.00 FMV per share at time of vesting $10.00 $10.00

Develop a risk management plan to implement strategies that minimize or eliminate risks, and protect your business with appropriate insurance coverage, such as liability, property and business interruption insurance. Get Help with TaxPlanningTaxplanning is a critical component of financial management.

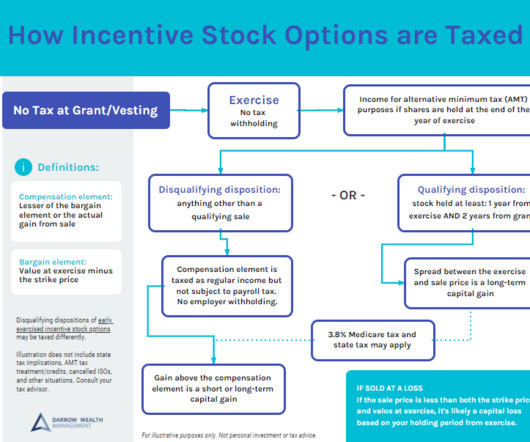

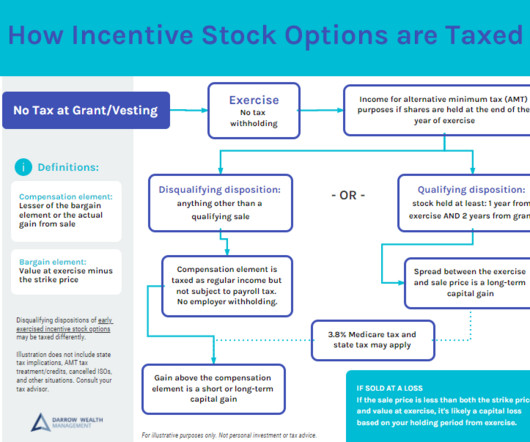

By Mike Valenti, CPA, CFP ® , Director, TaxPlanning Corporate executives often receive the brunt of the U.S. tax system. Typically, most or all of their income is W-2 income and subject to the higher ordinary tax rates as well as FICA taxes. The spread is taxed as ordinary wage income, subject to FICA taxes.

What are appropriate checklists for year-end taxplanning? Tax planners often develop checklists to guide taxpayers toward year-end strategies that might help reduce taxes. Certain tax benefits may be available if you can claim an individual as a dependent. Family taxplanning.

The sale of a business marks a major life event. With many sellers relying on the sale to fund their retirement and lifelong financial goals, getting it right from the start is critical. Getting professional help is key here as trying to negotiate a sale directly with a buyer might be short-sighted.

You will need to identify investment options for reinvestment of the proceeds that are similar to those you liquidate for tax purposes. Keep in mind the wash sale rule that would disallow the harvested loss if you repurchase the same investment within 30 days after the liquidation.

The surtax will increase the Massachusetts tax liability by $68,000 on the sale of their home. Further, both examples ignore other sources of income, such as wages, pre-tax retirement account distributions, dividends, etc., that could increase the tax due from the surtax. Consider an installment sale.

While tax-loss harvesting can be an effective way to increase your tax breaksand balance your portfolio in the processit’s important to observe IRS regulations regarding the strategy. Defer income where possible Strategically timing your income can have a major effect on your tax liability.

Charitable Giving and TaxPlanning The tax rules continue to encourage generosity. This means that in those years, you can contribute and deduct a total of $34,750, helping you to save more for retirement and save even more in taxes! These 2025 updates provide fresh chances to protect and grow your wealth.

Although there are a number of ways to accomplish a shifting of income, the following methods are most popular: employing family members, family partnerships, interest-free and below-market loans, gifting, sale- or gift-leaseback, trusts, and life insurance/annuities. Timing the receipt of your income can also help you lower your taxes.

For founders, employees, and executives with stock-based compensation, an 83(b) election can be a powerful taxplanning tool. When you make an 83(b) election, you’re opting to pay tax on unvested shares now, instead of when the stock vests. It can also preclude some taxplanning strategies down the road.

In this comprehensive guide, well examine tax-loss harvesting in depth, looking at its benefits, drawbacks, mechanics, and suitability for different types of investors. Table of Contents What is tax-loss harvesting? How does tax-loss harvesting work? What is the wash-sale rule? When should you avoid tax-loss harvesting?

This tax benefit is scheduled to sunset at the end of 2026. Taxplanning for 2026 Depending on your situation, income, and goals, your planning options will vary. As with anything in taxplanning, it’s important not to let the tax-tail wag the dog.

From quarterly estimated taxplanning to equity compensation and crypto taxplanning, diversifying your service offerings can not only set you apart from the competition, it can also help you significantly grow your revenue and retain clients.

Key Takeaways: A secondary sale allows private company shareholders, such as employees or early investors, to sell their shares to third-party buyers. It’s key to understand the tax implications of a secondary sale of private company stock. Table of Contents: What Is a Secondary Sale? How Does a Secondary Sale Work?

6 tax strategies for incentive stock options and AMT Triggering the alternative minimum tax isn’t the end of the world, but you don’t want to do it by accident. You’d have liquidity from the sale to pay any tax due in April. The cash crunch is quick to rain on a potential taxplanning parade.

Early sales of ISOs are taxed in the regular tax system. There are two AMT tax rates: 26% and 28%. AMT credits can only be used in years when not subject to the alternative minimum tax. At the end of the day, all of the taxplanning opportunities with ISOs involve risks.

Let’s look at two examples of NUA taxation based on the sale of employer securities post-NUA transfer date. These two examples result in separate taxation rules based on their dates of sale and highlight the need to incorporate taxplanning in NUA decisions. Watch to Learn More About Selecting Specific Lots for NUA.

Part 3: Tax-Wise Financial Planning In our last two pieces, we covered some tools of the tax-planning trade, as well as how to deploy them for tax-efficient investing. But taxplanning isn’t just for your investments. But we can weave each event into the tax-planning fabric of your financial life.

Part 3: Tax-Wise Financial Planning. In our last two pieces, we covered some tools of the tax-planning trade, as well as how to deploy them for tax-efficient investing. . But taxplanning isn’t just for your investments. Each can translate into tax-planning challenges and opportunities: .

It’s a masked sales call. Instead of coming to them with a sales pitch, come to them as an advocate. I just wanted to come in and do a seminar about how to do taxplanning in XYZ County. Treating the gatekeeper cold will cause you to lose sales. We have to get what I call “the second wave.” Take a longer term view.

6 tax strategies for incentive stock options and AMT Triggering the alternative minimum tax isn’t the end of the world, but you don’t want to do it by accident. You’d have liquidity from the sale to pay any tax due in April. The cash crunch is quick to rain on a potential taxplanning parade.

Mike Valenti, CPA, CFP ® , Director of TaxPlanning Tom Fridrich, JD, CLU, ChFC ® , Senior Wealth Planner It’s January, so it’s officially tax season! One of the most common client questions heard by tax preparers is, “So, what do you need from me?” The short answer to that question is often, “Everything.”

The upside of a well-timed exercise is clear: potential for significant tax savings and reducing the time you need to hold the stock to qualify for long-term capital gains tax rates. Unfortunately, for those tax savings to materialize, the post-IPO stock price at sale must be considerably more than the pre-IPO valuation at exercise.

The post Part 2: Tax-Wise Investment Techniques appeared first on Yardley Wealth Management, LLC. Part 2: Tax-Wise Investment Techniques In our last piece, we introduced some of the tools of the tax-planning trade. In other words, your tax-planning techniques matter at least as much as the tools.

The post Part 2: Tax-Wise Investment Techniques appeared first on Yardley Wealth Management, LLC. Part 2: Tax-Wise Investment Techniques. In our last piece, we introduced some of the tools of the tax-planning trade. In other words, your tax-planning techniques matter at least as much as the tools.

Real Estate Investment Taxation Real estate investments have the potential to generate rental income, appreciation, and tax benefits, but tax treatment varies depending on how the property is used. Rental Income: Taxed as ordinary income, but depreciation deductions can reduce taxable income.

A little bit of effort and forward thinking during our summer and fall months will lead to a much more palatable and, potentially, financially advantageous tax season the following year. The reason for this is quite simple – taxplanning requires actual planning.

For founders, employees, and executives with stock-based compensation, an 83(b) election can be a powerful taxplanning tool. When you make an 83(b) election, you’re opting to pay tax on unvested shares now, instead of when the stock vests. It can also preclude some taxplanning strategies down the road.

A good rule of thumb is to set aside at least 30% of every payment you receive to cover your estimated tax obligationshowever, this percentage may need to be adjusted based on your individual tax bracket. On the whole, its advisable to consult a tax adviso r to develop a dependable taxplan.

Their funds include Active funds, Absolute Funds, Liquid Funds, Overnight Funds, Gilt Funds, TaxPlans, Large Cap, Dynamic Asset Allocation Funds, and others. 26,644 crore, Quant ELSS Tax Saver Fund’s AUM of around Rs. 9,500 crore, Quant TaxPlan AUM is around Rs. It’s Sales declined by 6.89 3,936 crore.

If so, you’ve probably read about the alternative minimum tax (AMT), and qualifying and disqualifying dispositions. While AMT and holding periods for qualified sales may be important from a tax-reporting standpoint, they may be irrelevant if you simply exercise and sell your ISOs in a cashless transaction.

Video: Qualified Small Business Stock (QSBS) Explained QSBS tax benefits: excluding capital gains taxes If you have Section 1202 shares, the gain you’re able to exclude from federal long term capital gains tax at sale depends on your gain and the date the stock was acquired.

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content